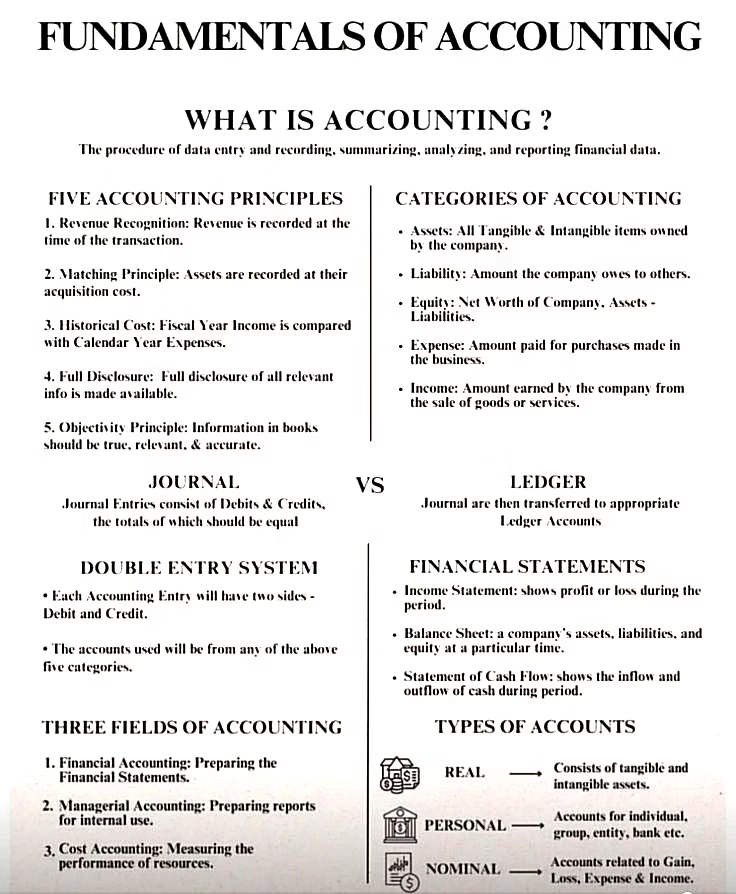

What Is An Account?

An account is a record of all business transactions under one room relating to a particular person, income expense, property, etc.

Accounts Can Be of Three Types:

Personal Account: Personal accounts consists of all those accounts which are directly related to a person, business firm, etc.

There are subtypes of personal accounts:

- Natural Person Account: A natural person account in accounting refers to the financial records of individual human beings, such as customers, suppliers, or the business owner. These accounts are used to track transactions and balances related to individuals with whom the business interacts. For example, Aaryaa Account, Aaryan Account.

- Artificial Personal Account: An artificial personal account in accounting represents legal entities that are not human beings but are treated as individuals for accounting purposes. These accounts include entities like companies, partnerships, banks, hospitals and government bodies. Essentially, they are created when a non-human entity is recognized as a separate legal entity in business dealings. For example, Company Account.

- Representative Personal Account: These accounts represent groups of individuals, like “salaries payable” which represents the amount owed to all employees. It represents owner’s Capital Account, Drawings Account.

- Related to Obligations/Entitlements: These accounts track amounts owed to or by the represented group or person, like outstanding salaries or prepaid expenses.

- Examples:

- Outstanding Salary Account: Represents salaries owed to employees for work already performed.

- Prepaid Expense Account: Represents expenses paid in advance for goods or services not yet received.

- Accrued Income Account: Represents income earned but not yet received.

- Income Received in Advance Account: Represents income received for goods or services not yet provided.

- Debtors Account: Represents amounts owed by customers for credit sales.

- Creditors Account: Represents amounts owed to suppliers.

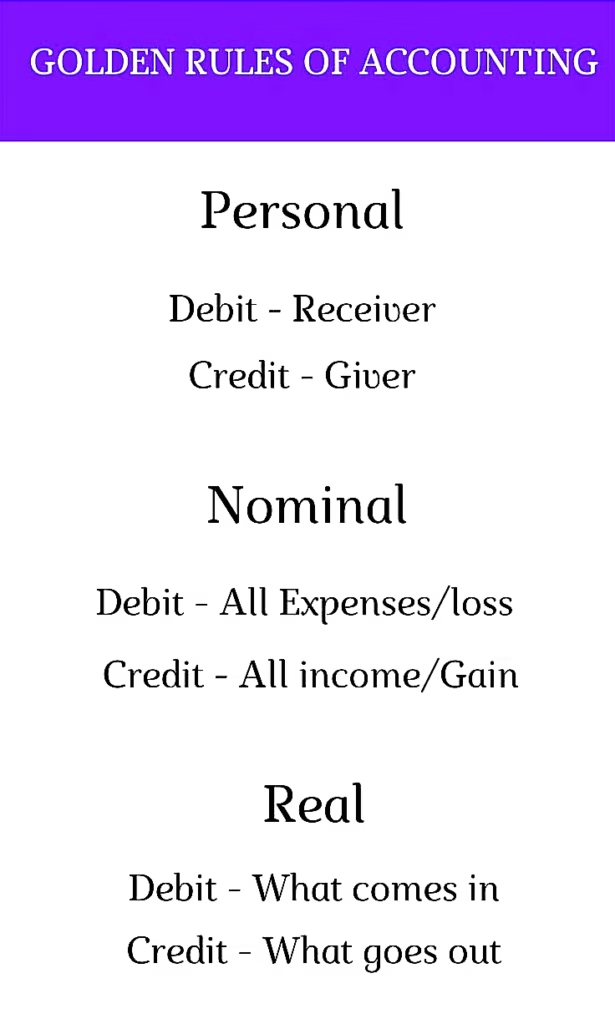

The “Golden Rule” for personal accounts is: “Debit the receiver, credit the giver”. This means that when a person receives something (e.g., cash, goods), their account is debited and when a person gives something (e.g., cash, goods), their account is credited.

For example, if a business sells goods to a customer on credit, the customer’s account (a natural personal account) would be debited for the amount owed. If the customer later pays the outstanding balance, their account would be credited.

Real Account: Real account consists of all the accounts related to assets like Plant and Machinery Account, Stock Account, Furniture and Fixtures Account, Cash Account and Stock Account.

Nominal Account: Nominal accounts consists of all those accounts which are related to Expenses, Losses, Incomes and Gaines like Rent Account, Printing and Stationery Account Advertisement Account.

Golden Rules of Accounting:

There are three golden rules in accounting to record business transactions each of these rules are associated with separate accounts.

- Personal Account: Debit the Receiver, Credit the Giver.

- Real Accounts: Debit what comes in, Credit what goes out.

- Nominal Accounts: Debit all Expenses and Losses, Credit all Incomes and Gains.

What Are Final Accounts?

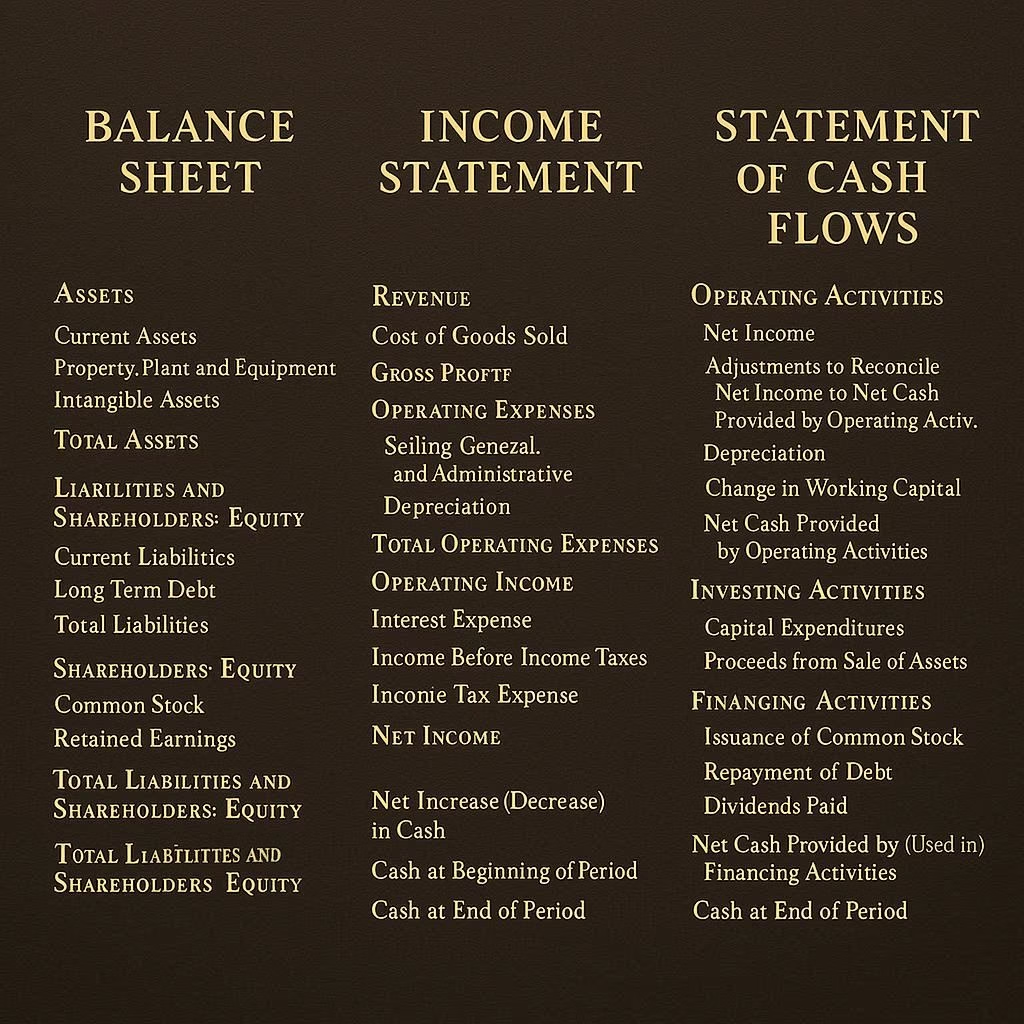

Final accounts, also known as financial statements, are a set of reports prepared at the end of an accounting period to summarize a company’s financial performance and position. They provide a comprehensive overview of a company’s financial health to stakeholders like management, owners, and investors. The main components of final accounts include the Trading and Profit & Loss Account and the Balance Sheet.

Final accounts, also known as financial statements, include the balance sheet, profit and loss account (or income statement), and cash flow statement. These statements provide a comprehensive overview of a company’s financial performance and position at the end of an accounting period.

Here’s a breakdown of each component:

Balance Sheet: A snapshot of a company’s assets, liabilities, and equity at a specific point in time, showing what the company owns, owes and the net worth of the business.

Profit and Loss Account (Income Statement): Summarizes a company’s revenues and expenses over a specific period, ultimately revealing the net profit or loss.

Cash Flow Statement: Tracks the movement of cash both into and out of a company, categorized into operating, investing and financing activities.

Key Components and their Purpose:

- Trading Account: This account determines the gross profit or loss from trading activities, essentially the buying and selling of goods.

- Profit and Loss Account: This account calculates the net profit or loss by considering all revenues and expenses, both direct and indirect, of the business.

- Balance Sheet: This statement presents a snapshot of a company’s assets, liabilities and equity at a specific point in time, revealing its financial position.

Objectives of Preparing Final Accounts:

- To determine profit or loss: Final accounts help in calculating the profitability of a business for a specific period.

- To assess financial position: They provide insights into the company’s assets, liabilities and overall financial health.

- To provide information to stakeholders: Final accounts serve as a crucial source of information for owners, investors, creditors and regulatory authorities.

- To ensure transparency and accountability: They facilitate transparency by disclosing financial performance and position to interested parties.

- To aid in decision-making: Final accounts help in making informed decisions regarding investments, financing and other business strategies.

- For compliance: They are essential for fulfilling legal and regulatory requirements.

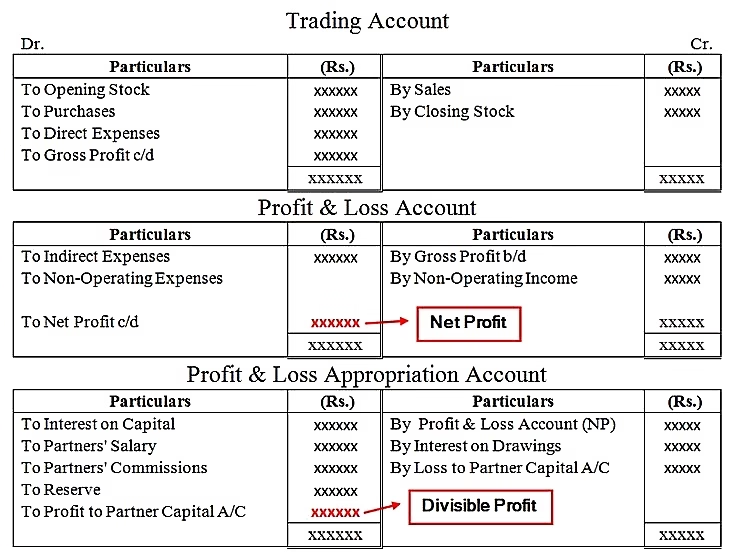

Trading Account:

Trading Account: Trading account is primarily prepared to know the gross profit or gross loss incurred as a result of trading activities of the business. In other words, in case of a manufacturing concern a manufacturing account is prepared to show the result of manufacturing activities, a trading account indicates buying and selling of goods.

If the amount of Sales exceeds the amount of purchases and the expenses directly connected with such purchases, the difference amount is termed as gross profit. On the contrary, if the purchases and direct expenses exceed the sales, the difference amount is known as gross loss. The sole purpose and ultimate objective of preparing the trading account is to find out the gross profit or gross loss of the business during a particular period.

A trading account is an account prepared to ascertain the gross profit or loss. It is a nominal account and represents the first stage of final accounts of a business which is prepared before the preparation of the Profit and Loss Account.

Objectives of Trading Account:

The preparation of trading account provides information about the gross profit and gross loss. It informs the gross profit of gross loss as a result of buying and selling the goods throughout the year. The percentage of current year gross profit on the amount of sales can be calculated and compared with those of the previous years. Thus, it inturn, provides data for comparison analysis and planning for a future period.

It provides necessary information about the direct expenses:

It provides information concerning gross profit: The percentage of gross profits on the amount of sales will show the success of the business. With the help of this financial ratio of gross profit to sales, a potential stakeholder can ascertain accurate comparison and make viable business decisions.

Accurate recording of direct expenses: All the expenses in the purchase in manufacturing of goods are recorded in the trading account in summarised form. Percentages of such expenses on sales can be calculated and accurately compared with those of the previous years. It is a great way to help the management to control and rationalise the direct expenses.

Accurate comparison of closing stock with those of the previous years: Closing stock has to be valued and recorded in the trading account. This inventory can be compared with the closing stock or inventory of the previous years and if the stock shows an increasing trend the reasons can be studied and corrected.

It provides safety against possible losses: If the ratio of gross profit has decreased in comparison to any previous preceding years, the company is in the position to take effective measures to safeguard against future losses. The company can keep an accurate track of its expenses in correspondence to its profit margins and take correct steps for deviations, if any.

Preparation of Trading Account:

Trading account is a nominal account and all expenses which relate to either purchase or manufacturing of goods are written on the debit side of trading account.

The transactions written on the debit side of the trading account are:

Opening stock: The opening stock refers to the stock of goods remaining unsold at the end of the previous year is termed as the opening stock of the current year. In simple terms, the closing stock of the last year becomes opening stock of the current year. The opening stock primary includes opening stock of raw material, opening stock of semi-finished goods or the work-in-progress, opening stock of finished goods.

Purchase and Purchase Returns: The goods which have been bought for resale are termed as purchases and goods which are returns to suppliers are inturn, purchase returns or return outwards. Purchase account will be given on the debit side of the trial balance and purchase returns account given on the credit side of the trial balance. Purchase returns, if any, will be shown as a deduction from purchases on the debit side of the trading account. Purchases include cash as well as credit purchases.

Direct Expenses: All expenses incurred for purchasing the goods, right from bringing them to the warehouse and manufacturing of these goods are called as direct expenditures. Direct expenses include the following expenditures:

- Wages: Wages refer to the payments paid to workers who are directly engaged in the loading, unloading and production of goods and such wages are debited to the trading account.

Some important instructions to be noted up:

The accounting treatment for various types of various transactions is quite different and needs to be understood well.

If the items ‘wages and salaries’ is given, it will be shown on the trading account, whereas, if ‘salaries and wages’ is given, it will be shown on the profit and loss account debit side.

If wages are paid for bringing a new machinery or for its installation it will be added to the cost of machine and hence, will not be shown in the trading account, it will be treated as a capital expenditure.

Carriage inwards or carriage should be debited to trading account because these are primarily paid for bring in the goods to the factory or the place of the business. However, carriage or freight is paid on bringing an asset, the amount should be added to the asset account and must not be depoted to the trading account.

Manufacturing expenses incurred in the manufacture of goods are shown on the debit side of the trading account such as coal, gas, fuel, water, power, factory rent, factory lighting, factory wages, etc.

The transactions written on the credit side of the trading account are:

Sales and Sales Returns: Both cash and credit sales will be included in the sales. The sales account will be a credit balance, whereas, the sales return account or returns inwards account with a debit balance. Sales returns, if any, will be deducted out of the sales on the credit side of the trading account.

Closing stock: The goods remaining unsold at the end of the year is primarily known as a closing stock or inventory. It is valued at cost price or market price whichever is less. Includes the closing stock of raw material, closing stock of semi-finished goods and closing stock of finished goods. This closing stock becomes the opening stock for the next accounting period.

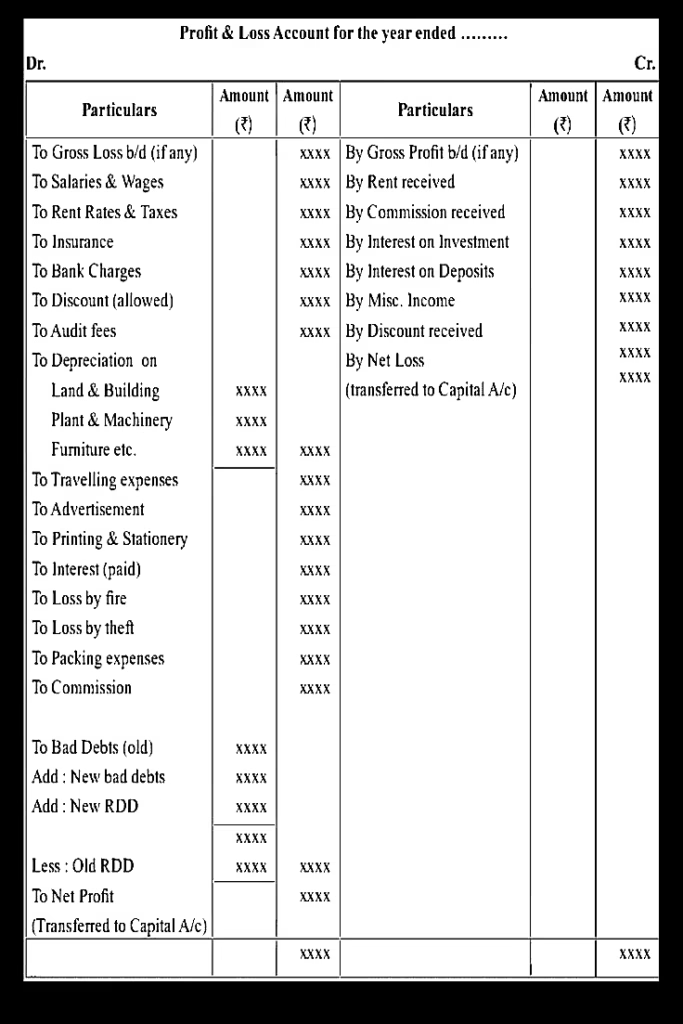

Profit And Loss Account:

A Profit And Loss Account is prepared to know the net profit or loss of the business. It is also a nominal account and represents second stage in the accounting procedure which is prepared after the praparation of the Trading Account.

Trading account only discloses the gross profit or gross loss on as a result of buying and selling of goods.

However, a business has to incurr a number of expenditures which are not taken into consideration in the trading account. The trading account deals with the transactions which are directly related to the core business and the manufacturing activities.

To know the accurate net profit or net loss incurred during the year a profit and loss account is prepared which contains all the items of losses and gains pertaining to the accounting year.

According to professor Carter, “A profit and loss account is an account into which all gains and losses are collected, in order to ascertain the excess gains over the losses or vice-versa.”

The Need and Importance of Profit And Loss Account:

For The Ultimate Determination of The Net Profit or Net Loss: A trading account only discloses the gross profit on or gross loss incurred as a result of trading or manufacturing activities within the business whereas, the profit and loss account discloses the net profit or net loss of the company.

Comparison With Previous Years’ Profit: The net profit of the current year can be compared with that of the previous years for better ascertaining the way in which the business is performing. The net profit serves as the greatest financial metric to get to know a clear vision and financial position of the business. It enables the top management to know whether the business is being conducted efficiently or not and steps to take to make it right.

Strategic Control on Expenses: Profit and loss account helps in comparing various expenses with the expenses of the previous years. The percentage of each individual expenses to net profit are calculated and compared with the similar ratio of previous years. Such financial metric comparison will be helpful in taking complete steps for controlling the necessary expenditures and improving the profitability and functioning of the business.

Future Profitability: The net profits of various years can be taken as a strong base for future profit-planning. It helps the business to efficiently and effectively allocate its resources and undertake future expansion.

Helpful In Preparation of The Balance Sheet: The Balance sheet can only be prepared after assertaining the net profit to the preparation of profit and loss account.

The Strategic Preparation of Profit And Loss Account:

A profit and loss account is started with the amount of gross profit or gross loss which is brought down from the trading account.

In simple terms, first the manufacturing expenses are taken into consideration and then the business expenses such as Office and Administrative Expenses, Selling and Distribution Expenses and Miscellaneous Expenses are taken into account.

All those expenses and losses which have not been debited to the trading account are now debited to the profit and loss account.

The expenses in profit and loss account primarily include administrative expenses, selling expenses, distribution expenses, etc. these are further classified as indirect expenses, the profit and loss account is a Nominal Account and all the expenses and losses are shown on its debit side and all the incomes and gains are shown on its credit side.

The transactions written on the Debit side of the Profit And Loss Account are:

Gross Loss: If the trading account shows gross loss it is shown on the debit side of the profit and loss account as gross loss broad down.

Office and Administrative Expenses : This primarily include salaries of the office employees, office rent, office lighting, postage, printing and stationery, legal charges, audit fees, etc.

Selling and Distribution Expenses: Advertisement charges, commission, carriage outwards, packaging charges, delivery expenses, etc.

Miscellaneous Expenses: Interest on loan, interest and capital charges, depreciation, etc

The transactions written on the Credit Side of the Profit And Loss Account are:

Gross Profit: The starting point of the credit side of the profit and loss account is the gross profit brought down from the trading account.

Other Incomes and Gains: All items of income and gains are shown on the credit side of the profit and loss account, which primarily include income from investments, rent received, discount received, commission earned, interest received, dividend received, etc.

If the credit side of the profit and loss account exceed that of the debit side, the different amount is termed as the net profit, on the contrary, the excess of debit side over the credit side is termed as net loss.

The net profit is added to the capital, whereas, the net loss is deducted from the capital.

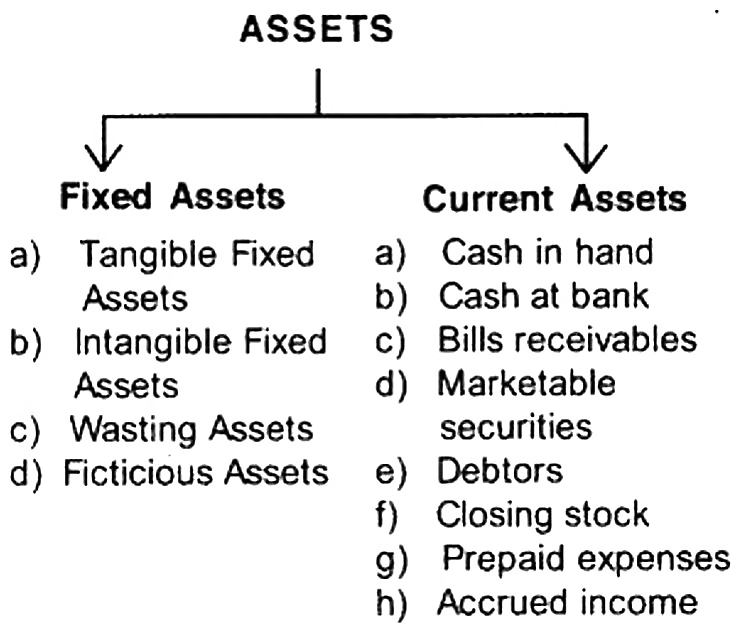

The Balance Sheet:

A balance sheet is a financial statement that contains details of a company’s assets or liabilities at a specific point in time. It is one of the three core financial statements.

The balance sheet is based on the fundamental equation: Assets = Liabilities + Equity.

A Balance Sheet is a statement of assets and liabilities at the end of the period. It shows the financial position of a business on a certain date and represents the third and final stage.

A Balance Sheet is prepared, as it displays the financial position of the business on a particular date to the owners as well as the potential stakeholders.

It helps the investors to know the earning capacity and financial health of the business.

A Balance Sheet is the statements which shows the true and fair view of the business as on a given date along with complete disclosure of contingencies, if any.

Contingent Liability is a potential obligation that may be incurred depending on the outcome of a probable future event. A contingent liability is one where the outcome of an existing event is uncertain and this uncertainty will be resolved by a future event.

The examples of contingent liabilities are: Disputed claims on liability under a damage suit, an unfavourable judgement of a court case, outstanding lawsuits, debts, product warranties, pending investigations, etc.

Features of The Balance Sheet:

- It is the final step in financial accounting.

- It is not an account under the double entry system- it is a statement.

- It has two sides- one side depits the assets held by the business whereas, the other shows the liabilities.

- It discloses the financial position and solvency of the business on a particular date.

- It is prepared after the praparation of the Trading and Profit and Loss Account as the net profit oe net loss of the business is included/reflected in the Balance Sheet through the Capital Account.

Presentation of A Balance Sheet:

Liquidity Preference Method: Under this method, the assets and liabilities are displayed in oder of their liquidity. The more liquid the assets, the earlier are they shown.

Premanency Preference Method: Under this method, the assets and liabilities are displayed in the Balance Sheet in order of their permanence. In simple terms, the more permanent the assets and liabilities, the earlier are they shown.

Parties Interested In Financial Statements:

In the recent years, the ownership of capital of many public limited companies has become truly broad based due to the dispersal of shareholding. Therefore, one may say that the public in general has become much more interested in financial statements. However, in addition to the shareholders, there are often stakeholders who are interested in the financial results disclosed by the annual reports of the company.

The various stakeholders of the company rely upon the financial statements published by the company to make their future business contracts and decisions. Such stakeholders include:

- Creditors.

- Potential suppliers.

- Debenture holders.

- Credit institutions like banks and various other financial institutions.

- Potential investors.

- Employees and trade unions.

- Important customers who wish to make a long standing contract with the company.

- Economist and investment analyst.

- Members of parliament, the public accounts committee and the estimates of committee in respect of Government companies.

- Exhibition authorities taxation.

- Other departments dealing with the industry in which the company is primarily engaged.

- The company law board.

- Various other stay holders who are interested within the company and look forward to make a solid investment and work with the company.

- Financial analyst.

Financial statements in today’s world has therefore, become a major and valuable factor for the parties interested in making a solid decision in regards to the company’s business.

Absolutely composed content material, Really enjoyed reading through.

“Thank you for your incredibly kind words and such a fantastic feedback, we really appreciate your kind words about the article and Simplfied Fiscal Affairs!”

Thanks for acknowledging the work put into this blog and the website.

The concept of accounts and financial statements is fundamental to understanding a company’s financial health. It’s interesting how different types of accounts, like personal and trading accounts, play unique roles in tracking transactions. The three golden rules of accounting seem essential for maintaining accuracy in financial records. Final accounts, such as the balance sheet and profit and loss statement, are crucial for stakeholders to assess performance. The explanation of gross profit and loss in the trading account is clear and insightful. However, how do companies ensure that these records are maintained consistently over time? What challenges do they face in keeping these accounts accurate, especially in large organizations with complex transactions?

Wir haben libersave in unser regionales Gutscheinsystem eingebunden. Es ist toll, wie einfach man verschiedene Anbieter auf einer Plattform bündeln kann. Whith regards, EUROB

Large organizations with complex transactions ensure consistency and accuracy in their financial records by implementing robust internal controls, leveraging sophisticated technology and conducting rigorous audits. Despite these measures, they face significant challenges, including a high volume of transactions, regulatory complexities and the risk of human error and fraud.

Understanding the intricacies of accounting is crucial for any business to maintain financial health. Your explanation of personal accounts and the golden rules of accounting provides a clear foundation for beginners. The distinction between debiting and crediting customer accounts highlights the importance of accurate record-keeping. The breakdown of final accounts, including the Trading Account, Profit & Loss Account, and Balance Sheet, offers valuable insights into a company’s financial performance. However, could you elaborate on how small businesses can effectively implement these accounting practices without overwhelming resources? I believe simplifying these concepts could help many entrepreneurs. Have you encountered challenges in applying these principles in real-world scenarios?

Wir haben libersave in unser regionales Gutscheinsystem eingebunden. Es ist toll, wie einfach man verschiedene Anbieter auf einer Plattform bündeln kann. Whith regards, PAYOL

Relatively small businesses in terms of scale, capital investment and expenditure can implement accounting practices by using user-friendly/ easy to understand and set up software, adopting simpler accounting methods like cash basis, prioritizing core tasks such as tracking income/expenses and cash flow, and considering external help from qualified bookkeepers or accountants for complex areas. Common challenges include lack of time, limited financial expertise and integrating accounting into daily operations.

For small businesses with limited resources, implementing effective accounting practices requires a simplified, systematic approach that prioritizes automation, regular reconciliation, and consistent routines. While challenges like limited financial expertise, cash flow issues and complex tax rules and regulations are common, they can be overcome by focusing on core tasks and implementing user-friendly tools.

Simplifying Accounting for Small Businesses

Use cloud-based accounting software: Many platforms offer user-friendly interfaces and automation, making it easier to manage finances without needing to be an accounting expert.

Adopt the cash basis accounting method: This method, which records income when received and expenses when paid, is simpler than the accrual basis, making it ideal for small businesses with simpler operations.

Prioritize core financial data: Focus on essential elements like tracking income and expenses, monitoring cash flow and understanding inventory. This provides a clear picture of the business’s financial health without getting involved in the complex details.

Separate business and personal finances: Keeping business and personal funds completely separate prevents confusion and makes tracking business transactions much easier and further profitability and tax liability becomes easy to assertain. .

Consider outsourcing: If time or expertise is limited, outsourcing tasks to a bookkeeper or professionally qualified accountant can be a resource-efficient solution.

Common Challenges & How to Address Them

Limited Resources (Time and Money):

Challenge: Small business owners often have limited budgets, making it hard to dedicate time or funds to accounting.

Solution: Leverage accounting software with affordable plans, focus on key metrics and explore outsourcing options for specific tasks rather than hiring a full-time employee.

Lack of Financial Expertise:

Challenge: Entrepreneurs may not have a deep understanding of accounting principles, leading to errors or an inability to interpret financial data correctly.

Solution: Choose user-friendly software, utilize online resources and courses for basic understanding, and partner with a professionally qualified accountant for tax preparation or complex financial decisions.

Integrating Accounting into Daily Operations:

Challenge: Accounting can feel like a separate, burdensome task rather than an integrated part of running the business.

Solution: Make financial tasks a regular part of the workflow by dedicating specific times each week for bookkeeping and use software that allows for mobile access and easy data entry on a continuous/regular basis.

I found this explanation of accounts and financial statements quite detailed and informative. It’s interesting how accounts are categorized and how transactions are recorded using specific rules. The breakdown of the trading account and its purpose clarifies how businesses track their performance. I wonder, though, how small businesses without dedicated accounting teams manage this process efficiently. Do you think automated tools have made financial management easier for everyone? Also, how do you ensure accuracy in recording transactions, especially when dealing with high volumes? It’s impressive how final accounts provide such a comprehensive view of a company’s financial health, but I’m curious—what happens if there’s an error in the financial statements? Wouldn’t that mislead stakeholders?

By the way, we’ve integrated libersave into our regional voucher system. It’s amazing how easy it is to bundle different providers on a single platform. Whith regards, TECHS

Small businesses manage accounting efficiently using automated software, which simplifies tasks, reduces errors and provides real-time financial insights. Automation improves accuracy by minimizing manual data entry and allows for systematic record-keeping, crucial for handling high-volume transactions. If an error exists in financial statements, stakeholders can be misled, making accuracy vital and requiring regular reconciliation and internal controls to catch and correct mistakes promptly.

Automated Tools for Small Business Financial Management:

Simplification & Efficiency: Automated accounting systems handle repetitive tasks like data entry, invoicing, and transaction tracking, freeing up time for owners to focus on growth rather than manual administration.

Improved Accuracy: By reducing human involvement in data input, automation significantly lowers the chance of manual errors, such as misplacing numbers or decimal points, leading to more accurate financial records.

Real-time Visibility: Automation provides immediate access to financial data, giving business owners a clear, up-to-date view of their cash flow, expenses and income, which aids in timely and informed decision-making.

Scalability: Reliable automated systems can grow with the business, ensuring that financial processes remain efficient even as transaction volumes increase.

Ensuring Transaction Accuracy with High Volumes:

Keep Detailed, Organized Records: Maintain all invoices, receipts and other supporting documents for every transaction to provide evidence for your financial records.

Use Integrated Accounting Software: Utilize software that can sync with other tools and automate the population of financial records, capturing data accurately and relating it to existing entries.

Implement Regular Reconciliations: Frequently compare your internal records with bank statements and other external financial data to identify and resolve discrepancies, if any, quickly.

Establish Internal Controls: Set up clear internal processes and checks to manage who handles financial information and how transactions are approved and recorded, which helps prevent errors and fraud.

Handling Errors in Financial Statements:

Leads to Misleading Stakeholders: Incorrect financial statements can give a false impression of a company’s financial health, leading to inaccurate decisions by various stakeholders like investors, creditors and management.

Requires Correction and Disclosure: If an error is discovered after statements are published, it must be corrected. Depending on the error’s significance, this might involve reissuing the financial statements or providing an explanation to affected stakeholders. The accounting principle of Complete Disclosure comes into play, which states that companies should completely disclose all the transactions and events taken place which impact the decision of the company’s stakeholders and it’s financial implications.

Best Practice is Prevention: The most effective way to deal with errors is to implement strong preventative measures, such as regular reconciliation, detailed record-keeping and rigorous internal controls, to minimize the risk of errors in the first place.

Key takeaways:

Automation is transforming financial management, especially for small businesses, by improving efficiency and accuracy.

Strong internal controls, reliable software, and consistent practices are essential for preventing and detecting errors.

Inaccurate financial statements can mislead stakeholders and have serious financial, legal, and reputational consequences.

Good takeaways

Simplified Fiscal Affairs really appreciates that, it gives us immense motivation and inspiration to keep moving forward and to come up with the best possible content.