Finance is a vast subject matter, it is a business language in which investors, businesses and the global economies communicate and interact with. Financial mastery and literacy ultimately impowers one to strategically make the best financial decisions and create the best possible financial outcomes. You are the creator of your reality! Respect the knowledge you are seeking today and tomorrow it will respect you..!

Effective Tax Planning-

An investor may pursue certain investments in order to adopt tax minimisation or as a part of his or her investment strategy. Tax planning is a method of availing certain tax exemptions and deductions through a legal procedure. A highly paid executive wants to make investments with a favourable tax treatment in order to lesser his or her overall income tax burden.

Taxes can eat your potential returns, but tax-efficient investing can help you hold on to more of what you’ve earned. By strategically choosing the right accounts, assets and timing, you can maximize returns while minimizing tax liabilities. Tax-efficient investing aims to maximize after-tax returns by minimizing tax liabilities. Tax-managed funds, bonds, and Treasury bonds are common tax-efficient investment vehicles. Tax-efficient investing is a strategy to use specific products and financial securities in a portfolio to maximize returns and legally & ethically minimize the taxes paid on those returns. Investing in the best high quality asset classes, high risk-high return assets is merely not sufficient, one has to make sure the amount of deductible tax.

Tax is a payment which is to be mandatorily paid on the income generated. The investor has to think logically and rationally in terms of making a wise, cost efficient and high return investment. The investment must be done with a diversified approach, do not invest a major amount in a single high risk- high return asset, instead opt for tax effective investment asset classes, these not only yield significant returns but also ensure to provide reasonable tax benefits. Investments in tax savings mutual funds is one of the examples of making a tax efficient investment.

Tax Planning Strategies for Individuals: Minimizing Liability

Tax planning is an essential aspect of personal finance, helping you minimize liability and maximize savings:

Tax planning is the legal financial process of analyzing your finances to minimize tax liability by strategically using legal deductions, exemptions and benefits available under tax laws, helping you save money, build wealth and meet financial goals like retirement, through choices like investing in tax-saving instruments (PPF, ELSS) or claiming home loan interest. It’s a proactive, year-round activity that ensures you pay the least amount legally possible, unlike tax evasion and involves understanding options like different tax regimes.

Here is a brief article in regards to the various exemptions and deductions an individual can claim legally through effective tax planning.

Understand Tax Slabs:

1. Know your slab: Familiarize yourself with income tax slabs and rates.

2. Optimize deductions: Claim eligible deductions to reduce taxable income.

Utilize Tax-Saving Instruments:

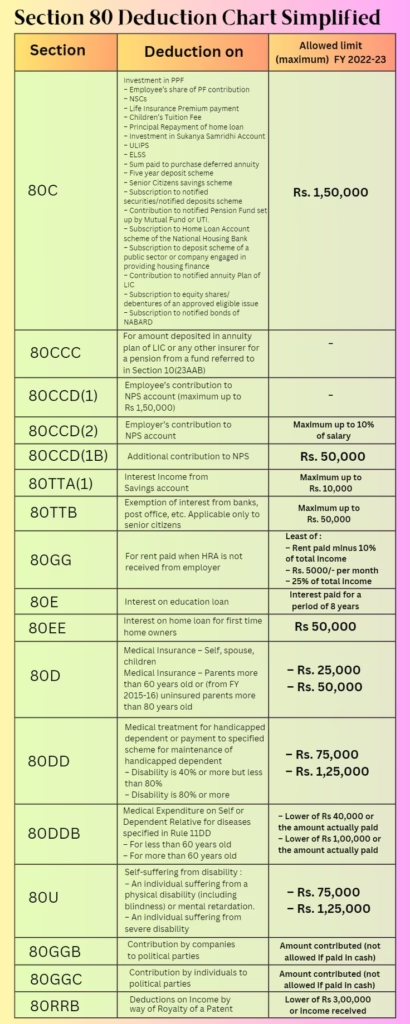

1. Section 80C: Invest in ELSS, PPF, NSC, or tax-saving FDs.

2. Section 80D: Claim health insurance premiums as deductions.

3. Section 16: Deductions for Income Under The Head Salaries:

- Standard Deduction (Section 16(ia)):

- A fixed amount of ₹50,000 is deducted from your gross salary.

- Available to all salaried employees and pensioners.

- It simplifies tax calculation and doesn’t require proof of expense.

- Entertainment Allowance Deduction (Section 16(ii)):

- Only for Central/State Government employees who receive this allowance.

- Deduction is the least of:

- ₹5,000.

- 20% of basic salary.

- The actual entertainment allowance received.

- Professional Tax (Section 16(iii)):

- Tax levied by state governments on employment/profession.

- You can deduct the actual amount paid during the year, up to a maximum of ₹2,500.

- If paid by the employer, it’s added to salary first and then deducted.

4. Section 24: Claim home loan interest as deductions.

Leverage Tax Benefits:

1. HRA exemptions: Claim House Rent Allowance exemptions.

2. Standard deduction: Claim standard deductions on salary income.

3. Tax credits: Claim tax credits for specified investments.

Plan for Long-Term Savings:

1. Retirement planning: Invest in NPS or retirement plans.

2. Education planning: Utilize tax benefits on education loans.

Section 80C Investments:

1. ELSS: Equity-linked savings schemes offer tax benefits and growth potential.

2. PPF: Public Provident Fund offers stable returns and tax benefits.

3. NSC: National Savings Certificate offers fixed returns and tax benefits.

4. Tax-saving FDs: Fixed deposits with tax benefits.

Health Insurance and Tax Benefits:

1. Section 80D: Claim deductions on health insurance premiums.

2. Preventive healthcare: Invest in preventive healthcare for tax benefits.

Home Loan and Tax Benefits:

1. Section 24: Claim home loan interest as deductions.

2. Principal repayment: Claim principal repayment as deductions under Section 80C.

Retirement Planning and Tax Benefits:

1. NPS: National Pension System offers tax benefits and retirement savings.

2. Retirement plans: Invest in retirement plans for tax benefits and savings.

The bottom line is, investing money is crucial to yield significant returns to beat inflation and generate a rate of return greater than the inflation rate to maintain or increase your purchasing power. Investment again is a crucial decision, it needs to be made taking into consideration the various financial parameters like risks & rewards, liquidity, tax liability, probable future estimated performances of the asset class and the economy at large.

By executing these advanced tax planning techniques, you can legally optimize your tax liability and maximize savings.