WHAT IS AUDIT?

“Audit is an examination of accounting records, undertaken with a view to establishing whether they correctly and completely reflect the transactions to which they purport to relate.” Prof. Dickers

“Auditing is concerned with the verification of accounting data, determining the accuracy and reliability of accounting statements and reports.” R.R. Mautz

“Long range objectives of an Audit should be to serve as a guide to management's future decisions in all financial matters such as controlling, forecasting, analysing and reporting. These objectives help the business unit to improve its performance.” Arthur W. Holme

- Auditing is nothing but the systematic and critical examination and verification of the books of accounts. It can be undertaken throughout the year or periodically.

- The primary aim is to find out whether the financial statements exhibit a true and fair view of the business.

- Origin of the term audit is said to be in the Latin term audire which means to listen.

- Audit of accounts by a duty qualified chartered accountant is mandatory for the registered joint stock companies, public trusts, bigger co-operative societies and for income tax and VAT tax payers above a particular limit.

Objectives of Audit:

- To find the reliability of the financial position and profit and loss statement.

- To check whether the financial statements of the company present a true and fair view.

- To check whether the financial statements are kept as per the provisions of the relevant Act.

- Verification of the entries with the relevant documentary evidences.

- To check whether all the money received is accounted for or not and all the payments made have proper supporting documents.

- To conduct an independent review of financial statements.

- Auditor has to examine the prevailing internal control and internal check systems prevalent in the organisation and must check the arithmetical accuracy of the books of accounts.

- The auditor has to check the physical existence of various assets shown in the balance sheet and check whether they present a true and fair value.

- After checking the accounts the auditor has to express his or her personal judgement on the maintenance of the books of accounts.

- The company who audits its financial statements on a timely basis builds a good reputation and goodwill.

- Helps the stakeholders with decision making as audited accounts are considered more reliable.

- To detect and prevent frauds and errors.

The main difference between the two (frauds and errors) is that errors are generally committed due to lack of knowledge and are considered to be innocent, whereas, frauds are committed intentionally.

1. INTRODUCTION TO FINANCIAL AUDIT

A financial audit is a systematic, independent, and evidence-based examination of an entity’s financial statements to determine whether they present a true and fair view in accordance with applicable accounting standards (e.g., IFRS, GAAP).

🔑 Core Objective

- Provide reasonable assurance

- Detect material misstatements due to:

- Fraud

- Error

- Enhance credibility of financial information for stakeholders

👥 Key Stakeholders

- Investors & shareholders

- Creditors & banks

- Regulators (SEBI, RBI, etc.)

- Management

2. FUNDAMENTAL CONCEPTS IN AUDITING

(A) True and Fair View

Financial statements must reflect the economic reality, not just legal compliance. They should completely disclose all the material facts and the true financial position of the business

(B) Materiality

- Threshold beyond which misstatements influence decisions

- Types:

- Quantitative (₹ amount)

- Qualitative (fraud, compliance breach)

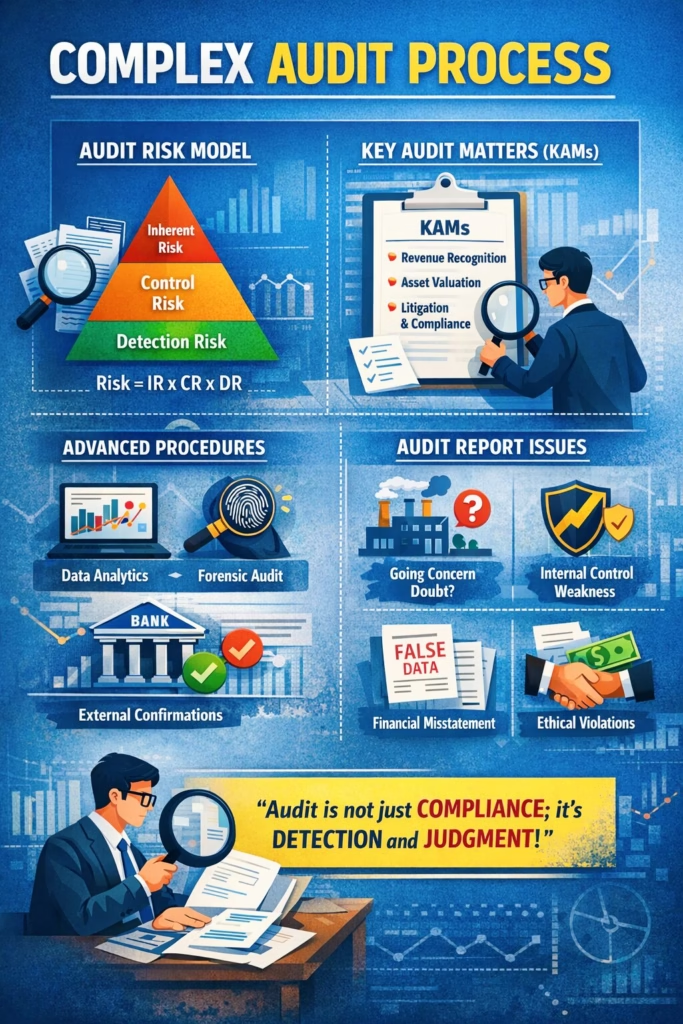

(C) Audit Risk Model

Audit risk = Risk of giving wrong opinion

It consists of:

- Inherent Risk (IR) – Natural susceptibility to misstatement

- Control Risk (CR) – Failure of internal controls

- Detection Risk (DR) – Auditor fails to detect error

👉 Relationship:

Audit Risk = IR × CR × DR

(D) Reasonable Assurance

Auditors provide high but not absolute assurance due to:

- Sampling limitations

- Judgement involved

- Time constraints

3. TYPES OF FINANCIAL AUDIT

1. External Audit

- Conducted by independent auditors

- Mandatory for companies

2. Internal Audit

- Conducted within organization

- Focus on risk management and controls

3. Statutory Audit

- Required by law (Companies Act, 2013 in India)

4. Forensic Audit

- Focus on fraud detection and investigation

4. AUDITING STANDARDS & FRAMEWORK

Audits are governed by professional standards:

🌍 International

- ISA (International Standards on Auditing)

🇮🇳 India

- Standards on Auditing (SA) issued by ICAI

Key Standards:

- SA 200 – Overall objectives

- SA 315 – Risk assessment

- SA 330 – Responses to risk

- SA 500 – Audit evidence

These standards ensure consistency, quality and reliability.

5. COMPLETE AUDIT ROADMAP (STEP-BY-STEP)

🔷 PHASE 1: ENGAGEMENT & PRE-AUDIT ACTIVITIES

Key Activities:

- Evaluate auditor independence

- Client acceptance/continuance

- Issue Engagement Letter

Engagement Letter Includes:

- Scope of audit

- Responsibilities

- Reporting framework

🔷 PHASE 2: AUDIT PLANNING

Planning is the foundation of audit quality.

Activities:

- Understand business environment

- Identify industry risks

- Review prior audits

- Set materiality level

- Develop audit strategy

Output:

✔ Audit Plan

✔ Audit Program

Planning ensures efficient allocation of audit resources.

🔷 PHASE 3: RISK ASSESSMENT

Objective:

Identify risks of material misstatement

Procedures:

- Inquiry with management

- Analytical procedures

- Observation & inspection

Analytical Procedures Example:

- Ratio analysis

- Trend analysis

These help identify unusual fluctuations.

🔷 PHASE 4: UNDERSTANDING INTERNAL CONTROL

Auditors evaluate:

- Control environment

- Risk assessment system

- Control activities

- Internal check and control systems

Outcome:

- Assess Control Risk

- Decide whether to rely on controls

🔷 PHASE 5: AUDIT EXECUTION (FIELDWORK)

This is the core phase of audit.

5.1 Tests of Controls

- Check effectiveness of internal controls

- Example:

- Approval systems

- Segregation of duties

5.2 Substantive Procedures

(A) Substantive Analytical Procedures

- Compare financial trends

- Identify abnormal financial and business activities

(B) Tests of Details

- Vouching transactions

- Verification of balances

- External confirmations

👉 Aim: Obtain sufficient and appropriate audit evidence

🔷 PHASE 6: AUDIT SAMPLING

Since full checking is impractical:

- Auditors use sampling techniques

Types:

- Statistical sampling

- Judgmental sampling

Risk:

Sampling may miss misstatements → increases detection risk

🔷 PHASE 7: EVALUATION OF EVIDENCE

Auditors assess:

- Sufficiency (quantity)

- Appropriateness (quality)

Key Considerations:

- Contradictions in evidence

- Reliability of sources

- Management bias

🔷 PHASE 8: COMPLETION & REVIEW

Final Procedures:

- Review subsequent events

- Going concern assessment

- Obtain written representations

- Evaluate misstatements

🔷 PHASE 9: AUDIT REPORTING

Final output = Auditor’s Opinion

Types of Audit Opinions:

| Type | Meaning |

|---|---|

| Unqualified (Clean) | True & fair view |

| Qualified | Minor issues |

| Adverse | Misleading statements |

| Disclaimer | Insufficient evidence |

6. ADVANCED AUDITING TECHNIQUES

🔹 1. Analytical Procedures

- Ratio analysis

- Regression models

- Data analytics

🔹 2. Computer Assisted Audit Techniques (CAATs)

- Data mining

- AI-based anomaly detection

🔹 3. Forensic Techniques

- Fraud detection

- Benford’s Law

🔹 4. Continuous Auditing

- Real-time auditing using IT systems

7. KEY AUDIT ASSERTIONS

Auditors verify financial statements based on assertions:

- Existence

- Completeness

- Accuracy

- Valuation

- Rights & Obligations

- Presentation & Disclosure

8. INTERNAL CONTROL & CORPORATE GOVERNANCE LINK

Strong internal control:

- Reduces audit risk

- Improves efficiency

Weak control:

- Requires extensive substantive testing

9. LIMITATIONS OF FINANCIAL AUDIT

- Based on sampling

- Relies on management data

- Cannot detect all fraud

- Time & cost constraints

10. PRACTICAL EXAMPLE (SIMPLIFIED)

Case: Manufacturing Company

- Auditor plans audit

- Identifies inventory as high-risk area

- Tests controls (inventory management system)

- Performs stock verification

- Uses sampling to test transactions

- Confirms balances with suppliers

- Issues clean/qualified report

11. COMPLETE FLOW SUMMARY (QUICK REVISION)

Engagement → Planning → Risk Assessment → Internal Control Review →

Execution (Testing) → Evidence Evaluation → Completion → Reporting

12. CONCLUSION

Financial auditing is a structured, risk-based, evidence-driven process designed to ensure the reliability of financial reporting. It integrates technical standards, analytical judgment and professional skepticism to provide assurance to stakeholders.

In modern environments, auditing is evolving toward:

- Data analytics

- AI-driven audits

- Continuous assurance

📘 CASE STUDY 1: Enron Corporation AUDIT FAILURE

🔷 1. Background

Enron Corporation was a major U.S.-based energy trading and utilities company, once ranked among the top corporations globally.

- Founded: 1985

- Headquarters: Houston, Texas

- Auditor: Arthur Andersen

🔷 2. Nature of Fraud

Enron used complex accounting techniques to hide debt and inflate profits.

Key Methods:

(A) Special Purpose Entities (SPEs)

- Created off-balance-sheet entities

- Transferred debt to these entities

- Result: Financial statements looked stronger than reality

(B) Mark-to-Market Accounting

- Recognized future profits immediately

- Unrealistic revenue recognition

(C) Manipulation of Financial Statements

- Inflated income

- Concealed liabilities

🔷 3. Role of Auditor: Arthur Andersen

Major Failures:

- Approved aggressive accounting policies

- Failed to question management assumptions

- Conflict of interest (consulting + audit fees)

- Destroyed key audit documents during investigation

👉 This violated the principle of auditor independence and professional skepticism

🔷 4. Collapse

- Year: 2001

- Losses: ~$74 billion shareholder value wiped out

- Thousands lost jobs and pensions

🔷 5. Audit Failures Identified

❌ Lack of Professional Skepticism

Auditors relied heavily on management representations

❌ Failure in Risk Assessment

Did not properly evaluate off-balance-sheet risks

❌ Weak Audit Evidence

Insufficient verification of SPE transactions

❌ Ethical Breach

Document shredding scandal

🔷 6. Consequences

- Arthur Andersen collapsed

- Introduction of Sarbanes-Oxley Act

- Stricter audit regulations globally

🔷 7. Key Lessons

✔ Independence is critical

✔ Complex transactions require deeper scrutiny

✔ Ethical responsibility > client relationship

✔ Strong internal controls must be verified

📘 CASE STUDY 2: Satyam Computer Services AUDIT FAILURE

🔷 1. Background

Satyam Computer Services was a leading Indian IT company.

- Founded: 1987

- Founder: Ramalinga Raju

- Auditor: PricewaterhouseCoopers

🔷 2. Nature of Fraud

The fraud was systematic financial statement manipulation over several years.

Key Frauds:

(A) Inflated Cash & Bank Balances

- Fake bank statements created

- Non-existent cash recorded

(B) Overstated Revenues

- Fake invoices

- Artificially increased profits

(C) Understated Liabilities

- Concealed obligations

👉 Total fraud: ~₹7,000 crore

🔷 3. Confession

In 2009, Ramalinga Raju confessed:

“It was like riding a tiger, not knowing how to get off without being eaten.”

🔷 4. Role of Auditor: PricewaterhouseCoopers

Major Failures:

- Did not independently verify bank balances

- Relied on forged documents

- Failed to perform external confirmations

- Ignored red flags (unusual profit margins)

🔷 5. Audit Failures Identified

❌ Failure in External Confirmation

Bank balances were not verified directly

❌ Over-Reliance on Management

Accepted documents without skepticism

❌ Weak Analytical Procedures

Ignored abnormal financial ratios

❌ Lack of Due Diligence

Did not detect fake invoices

🔷 6. Consequences

- Stock market crash for Satyam

- Arrest of key executives

- Ban and penalties on PricewaterhouseCoopers in India

- Strengthening of corporate governance norms in India

🔷 7. Regulatory Impact (India)

- Strengthening of Clause 49 (Corporate Governance)

- Increased ICAI oversight

- Improved auditing standards

🔷 8. Key Lessons

✔ Always verify bank confirmations independently

✔ Analytical procedures are essential

✔ Auditor skepticism must be strong

✔ Fraud can exist even in large companies

⚖️ COMPARATIVE ANALYSIS: ENRON vs SATYAM

| Aspect | Enron | Satyam |

|---|---|---|

| Type of Fraud | Off-balance sheet | Fictitious assets |

| Key Issue | Hidden liabilities | Fake cash balances |

| Auditor | Arthur Andersen | PwC |

| Nature of Failure | Complex accounting misuse | Basic audit negligence |

| Regulatory Impact | Sarbanes-Oxley Act | Strengthened Indian governance |

🎯 FINAL INSIGHT

Both cases highlight a critical truth:

Audit failure is rarely due to lack of knowledge — it is due to lack of skepticism, independence and ethical judgment.

🎓 VIVA QUESTIONS & ANSWERS – FINANCIAL AUDIT

🔷 BASIC CONCEPTUAL QUESTIONS

1. What is a Financial Audit?

A financial audit is an independent examination of financial statements to express an opinion on whether they present a true and fair view in accordance with applicable accounting standards.

2. What is meant by “True and Fair View”?

It means financial statements reflect the economic substance of transactions, are free from material misstatements, and are unbiased.

3. What is Audit Risk?

Audit risk is the risk that the auditor expresses an inappropriate opinion when financial statements are materially misstated.

4. What are components of Audit Risk?

Audit Risk=Inherent Risk×Control Risk×Detection Risk

- Inherent Risk (IR)

- Control Risk (CR)

- Detection Risk (DR)

5. What is Materiality?

Materiality is the threshold above which misstatements influence economic decisions of users.

6. Difference between Internal Audit and External Audit?

| Basis | Internal Audit | External Audit |

|---|---|---|

| Objective | Improve operations | Express opinion |

| Appointment | Management | Shareholders |

| Scope | Broad | Financial statements |

7. What is Professional Skepticism?

It is a questioning mindset where auditors critically assess audit evidence rather than blindly trusting management.

🔷 AUDIT PROCESS QUESTIONS

8. What are the main stages of an audit?

- Engagement

- Planning

- Risk Assessment

- Internal Control Evaluation

- Audit Execution

- Reporting

9. What is Audit Planning?

Audit planning involves developing an overall strategy and detailed approach to conduct the audit efficiently.

10. What are Audit Assertions?

Assertions are management claims embedded in financial statements:

- Existence

- Completeness

- Accuracy

- Valuation

- Rights & Obligations

11. What is Audit Evidence?

Audit evidence is information used by the auditor to form an opinion.

Types:

- Documentary

- Physical

- Analytical

- External confirmations

12. What are Substantive Procedures?

Procedures performed to detect material misstatements:

- Tests of details

- Analytical procedures

13. What is Audit Sampling?

Audit sampling involves examining less than 100% of data to draw conclusions about the entire population.

14. What is an Audit Report?

It is the final output where the auditor expresses an opinion on financial statements.

15. Types of Audit Opinions?

- Unqualified (Clean)

- Qualified

- Adverse

- Disclaimer

🔷 ADVANCED AUDIT QUESTIONS

16. What is Detection Risk?

Detection risk is the risk that audit procedures fail to detect existing material misstatements.

17. How do auditors reduce audit risk?

- Increasing sample size

- Performing more substantive tests

- Using reliable evidence

18. What are Analytical Procedures?

Evaluation of financial data through relationships and trends (ratios, comparisons).

19. What are CAATs?

Computer Assisted Audit Techniques used for data analysis and fraud detection.

20. What is Going Concern Concept?

It assumes the business will continue operations for the foreseeable future.

🔷 CASE STUDY VIVA – ENRON

About Enron Corporation

21. What was the Enron scandal?

A major accounting fraud where liabilities were hidden using off-balance-sheet entities.

22. What are Special Purpose Entities (SPEs)?

Separate legal entities used to move debt off the company’s balance sheet.

23. Which auditor was involved in Enron?

Arthur Andersen

24. What was the main audit failure in Enron?

Failure to challenge complex accounting practices and lack of independence.

25. What is Mark-to-Market Accounting?

Recording assets at current market value, even if profits are unrealized.

26. What lesson did Enron teach auditors?

Importance of:

- Independence

- Ethical behavior

- Strong skepticism

27. What law was introduced after Enron?

Sarbanes-Oxley Act

🔷 CASE STUDY VIVA – SATYAM

About Satyam Computer Services

28. What was the Satyam scam?

A corporate fraud involving inflated cash balances and fake revenues.

29. Who was the key person behind Satyam fraud?

Ramalinga Raju

30. Which audit firm audited Satyam?

PricewaterhouseCoopers

31. What was the major audit failure in Satyam?

Failure to independently verify bank balances.

32. What basic audit procedure was ignored?

External confirmation of bank balances.

33. What were the red flags ignored?

- High profit margins

- Unusual cash balances

- Inconsistent financial ratios

34. What lesson does Satyam provide?

Even basic audit procedures, if ignored, can lead to massive fraud.

🔷 CRITICAL THINKING QUESTIONS (HIGH SCORING)

35. Why do audit failures occur despite standards?

- Lack of independence

- Over-reliance on management

- Ethical lapses

- Time and cost pressures

36. Can audit guarantee fraud detection?

No. Audit provides reasonable assurance, not absolute assurance.

37. Which is more dangerous: Enron-type or Satyam-type fraud?

- Enron → Complex manipulation

- Satyam → Basic control failure

👉 Both are equally dangerous in different ways

38. How can audit quality be improved?

- Strong governance

- Auditor rotation

- Use of technology

- Strict regulations

🎯 FINAL VIVA TIP

If examiner asks ANY question, structure your answer like:

👉 Definition → Concept → Example → Conclusion