WHAT IS AUDIT?

“Audit is an examination of accounting records, undertaken with a view to establishing whether they correctly and completely reflect the transactions to which they purport to relate.” Prof. Dickers

“Auditing is concerned with the verification of accounting data, determining the accuracy and reliability of accounting statements and reports.” R.R. Mautz

“Long range objectives of an Audit should be to serve as a guide to management's future decisions in all financial matters such as controlling, forecasting, analysing and reporting. These objectives help the business unit to improve its performance.” Arthur W. Holme

- Auditing is nothing but the systematic and critical examination and verification of the books of accounts. It can be undertaken throughout the year or periodically.

- The primary aim is to find out whether the financial statements exhibit a true and fair view of the business.

- Origin of the term audit is said to be in the Latin term audire which means to listen.

- Audit of accounts by a duty qualified chartered accountant is mandatory for the registered joint stock companies, public trusts, bigger co-operative societies and for income tax and VAT tax payers above a particular limit.

Objectives of Audit:

- To find the reliability of the financial position and profit and loss statement.

- To check whether the financial statements of the company present a true and fair view.

- To check whether the financial statements are kept as per the provisions of the relevant Act.

- Verification of the entries with the relevant documentary evidences.

- To check whether all the money received is accounted for or not and all the payments made have proper supporting documents.

- To conduct an independent review of financial statements.

- Auditor has to examine the prevailing internal control and internal check systems prevalent in the organisation and must check the arithmetical accuracy of the books of accounts.

- The auditor has to check the physical existence of various assets shown in the balance sheet and check whether they present a true and fair value.

- After checking the accounts the auditor has to express his or her personal judgement on the maintenance of the books of accounts.

- The company who audits its financial statements on a timely basis builds a good reputation and goodwill.

- Helps the stakeholders with decision making as audited accounts are considered more reliable.

- To detect and prevent frauds and errors.

The main difference between the two (frauds and errors) is that errors are generally committed due to lack of knowledge and are considered to be innocent, whereas, frauds are committed intentionally.

🔷 BASIC CONCEPTUAL QUESTIONS

1. What is a Financial Audit?

A financial audit is an independent examination of financial statements to express an opinion on whether they present a true and fair view in accordance with applicable accounting standards.

2. What is meant by “True and Fair View”?

It means financial statements reflect the economic substance of transactions, are free from material misstatements and are unbiased.

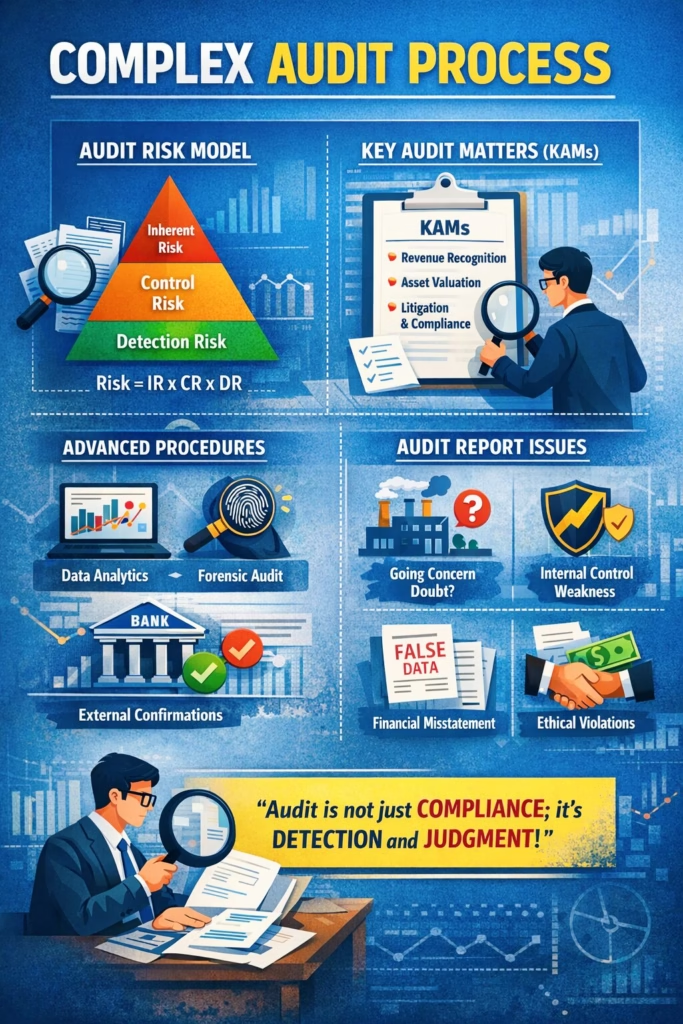

3. What is Audit Risk?

Audit risk is the risk that the auditor expresses an inappropriate opinion when financial statements are materially misstated.

4. What are components of Audit Risk?

Audit Risk=Inherent Risk×Control Risk×Detection Risk

- Inherent Risk (IR)

- Control Risk (CR)

- Detection Risk (DR)

5. What is Materiality?

Materiality is the threshold above which misstatements influence economic decisions of users.

6. Difference between Internal Audit and External Audit?

| Basis | Internal Audit | External Audit |

|---|---|---|

| Objective | Improve operations | Express opinion |

| Appointment | Management | Shareholders |

| Scope | Broad | Financial statements |

7. What is Professional Skepticism?

It is a questioning mindset where auditors critically assess audit evidence rather than blindly trusting management.

🔷 AUDIT PROCESS QUESTIONS

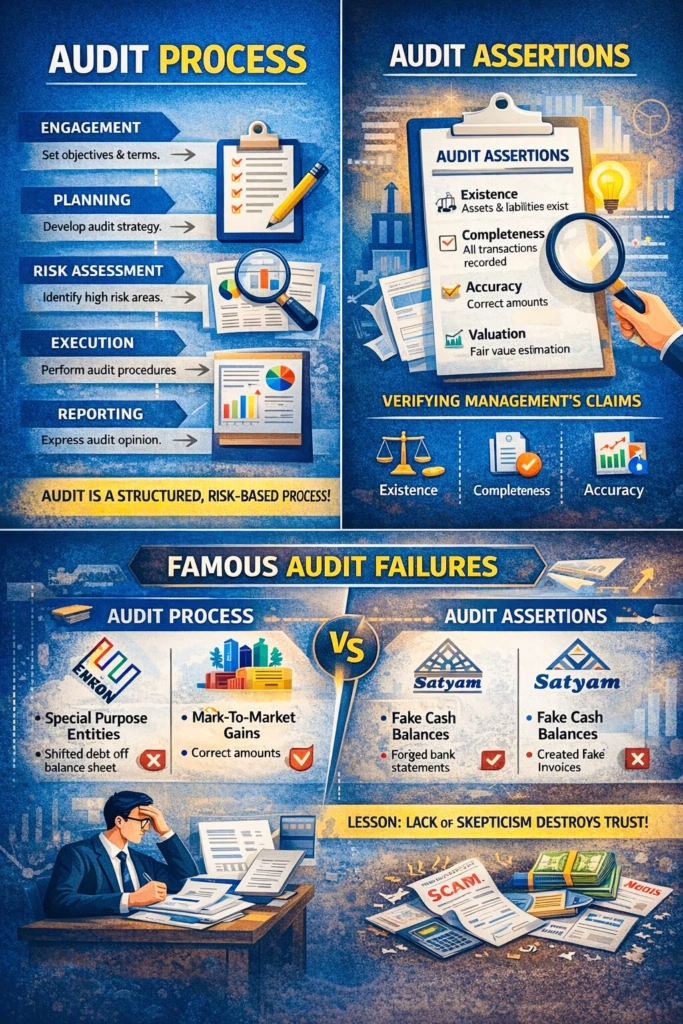

8. What are the main stages of an audit?

- Engagement

- Planning

- Risk Assessment

- Internal Control Evaluation

- Audit Execution

- Reporting

9. What is Audit Planning?

Audit planning involves strategically developing an overall strategy and detailed approach to conduct the audit efficiently.

10. What are Audit Assertions?

Assertions are management claims embedded in financial statements:

- Existence

- Completeness

- Accuracy

- Valuation

- Rights & Obligations

11. What is Audit Evidence?

Audit evidence is information used by the auditor to form an opinion.

Types:

- Documentary

- Physical

- Analytical

- External confirmations

12. What are Substantive Procedures?

Procedures performed to detect material misstatements:

- Tests of details

- Analytical procedures

13. What is Audit Sampling?

Audit sampling involves examining less than 100% of data to draw conclusions about the entire population.

14. What is an Audit Report?

It is the final output where the auditor expresses an opinion on financial statements.

15. Types of Audit Opinions?

- Unqualified (Clean)

- Qualified

- Adverse

- Disclaimer

🔷 ADVANCED AUDIT QUESTIONS

16. What is Detection Risk?

Detection risk is the risk that audit procedures fail to detect existing material misstatements.

17. How do auditors reduce audit risk?

- Increasing sample size

- Performing more substantive tests

- Using reliable evidence

- Continuous and thorough check

- Surprise visits

- Checking the internal control systems prevalent and their reliability

- Checking for any previous history of accounting errors or financial frauds.

- Demanding all the required documentation and information for the audit.

- Keeping a data and system driven approach to effectively execute the audit procedure.

18. What are Analytical Procedures?

Evaluation of financial data through relationships and trends (ratios, comparisons).

19. What are CAATs?

Computer Assisted Audit Techniques used for data analysis and fraud detection.

20. What is Going Concern Concept?

It assumes the business will continue operations for the foreseeable future.

🔷 CASE STUDY VIVA – ENRON

About Enron Corporation

21. What was the Enron scandal?

A major accounting fraud where liabilities were hidden using off-balance-sheet entities.

22. What are Special Purpose Entities (SPEs)?

Separate legal entities used to move debt off the company’s balance sheet.

23. Which auditor was involved in Enron?

Arthur Andersen

24. What was the main audit failure in Enron?

Failure to challenge complex accounting practices and lack of independence.

25. What is Mark-to-Market Accounting?

Recording assets at current market value, even if profits are unrealized.

26. What lesson did Enron teach auditors?

Importance of:

- Independence

- Ethical behavior

- Strong skepticism

27. What law was introduced after Enron?

Sarbanes-Oxley Act

🔷 CASE STUDY VIVA – SATYAM

About Satyam Computer Services

28. What was the Satyam scam?

A corporate fraud involving inflated cash balances and fake revenues.

29. Who was the key person behind Satyam fraud?

Ramalinga Raju

30. Which audit firm audited Satyam?

PricewaterhouseCoopers

31. What was the major audit failure in Satyam?

Failure to independently verify bank balances.

32. What basic audit procedure was ignored?

External confirmation of bank balances.

33. What were the red flags ignored?

- High profit margins

- Unusual cash balances

- Inconsistent financial ratios

34. What lesson does Satyam provide?

Even basic audit procedures, if ignored, can lead to massive fraud.

🔷 CRITICAL THINKING QUESTIONS (HIGH SCORING)

35. Why do audit failures occur despite standards?

- Lack of independence

- Over-reliance on management

- Ethical lapses

- Time and cost pressures

36. Can audit guarantee fraud detection?

No. Audit provides reasonable assurance, not absolute assurance.

37. Which is more dangerous: Enron-type or Satyam-type fraud?

- Enron → Complex manipulation

- Satyam → Basic control failure

👉 Both are equally dangerous in different ways

38. How can audit quality be improved?

- Strong governance

- Auditor rotation

- Use of technology

- Strict regulations

🎯 FINAL VIVA TIP

If examiner asks ANY question, structure your answer like:

👉 Definition → Concept → Example → Conclusion