Finance is a vast subject matter, it is a beautiful language in which investors, businesses and the global economies communicate and interact with. Financial mastery and literacy ultimately impowers one to strategically make the best financial decisions and create the best possible financial outcomes. You are the creator of your reality! Respect the knowledge you are seeking today and tomorrow it will respect you..!

Risk:

Risk is a component which follows every investment. Higher the risk, higher will be the rate of return and vice versa.

Risk management plays an integral role in the business setting. Identifying and evaluating various financial risks relating to operational, credit, market risk, etc. The investor has to use various tools in order to reduce the risk associated and create risk management methods like investment in sound/reliable and creditworthy financial securities and insurances.

1. Introduction to Financial Risk Management

Financial Risk Management (FRM) is a systematic and scientific approach to identifying, measuring, analyzing and controlling financial uncertainties that can negatively impact an organization’s value.

At its core, FRM aims to:

Protect capital

Stabilize earnings

Enhance decision-making under uncertainty

In modern finance, FRM evolved from portfolio theory (Harry Markowitz, 1952) and has now become a strategic function, not just a defensive tool.

In simple terms:

In simple terms:

FRM ensures that risks are understood, quantified and managed—not avoided blindly.

2. Nature and Sources of Financial Risk

Financial risk arises due to uncertainty in financial markets, operations and counterparties.

Key Characteristics:

- Dynamic and interconnected

- Measurable (quantitatively or qualitatively)

- Influenced by macroeconomic and internal factor

3. Types of Financial Risks (Core Classification)

3.1 Market Risk

Risk of losses due to market price fluctuations:

- Interest rate risk

- Foreign exchange (FX) risk

- Equity price risk

- Commodity risk

Example: Rising interest rates reduce bond prices.

3.2 Credit Risk

Risk that a borrower fails to repay obligations.

Includes:

- Default risk

- Counterparty risk

- Settlement risk

Measured via:

- Probability of Default (PD)

- Loss Given Default (LGD)

- Exposure at Default (EAD)

3.3 Liquidity Risk

Inability to meet short-term financial obligations.

Types:

- Funding liquidity risk

- Market liquidity risk

3.4 Operational Risk

Loss due to:

- System failures

- Fraud

- Human error

- External events

3.5 Advanced Risk Types

- Model Risk (errors in risk models)

- Systemic Risk (entire financial system collapse)

- Reputational Risk

- Legal & Compliance Risk

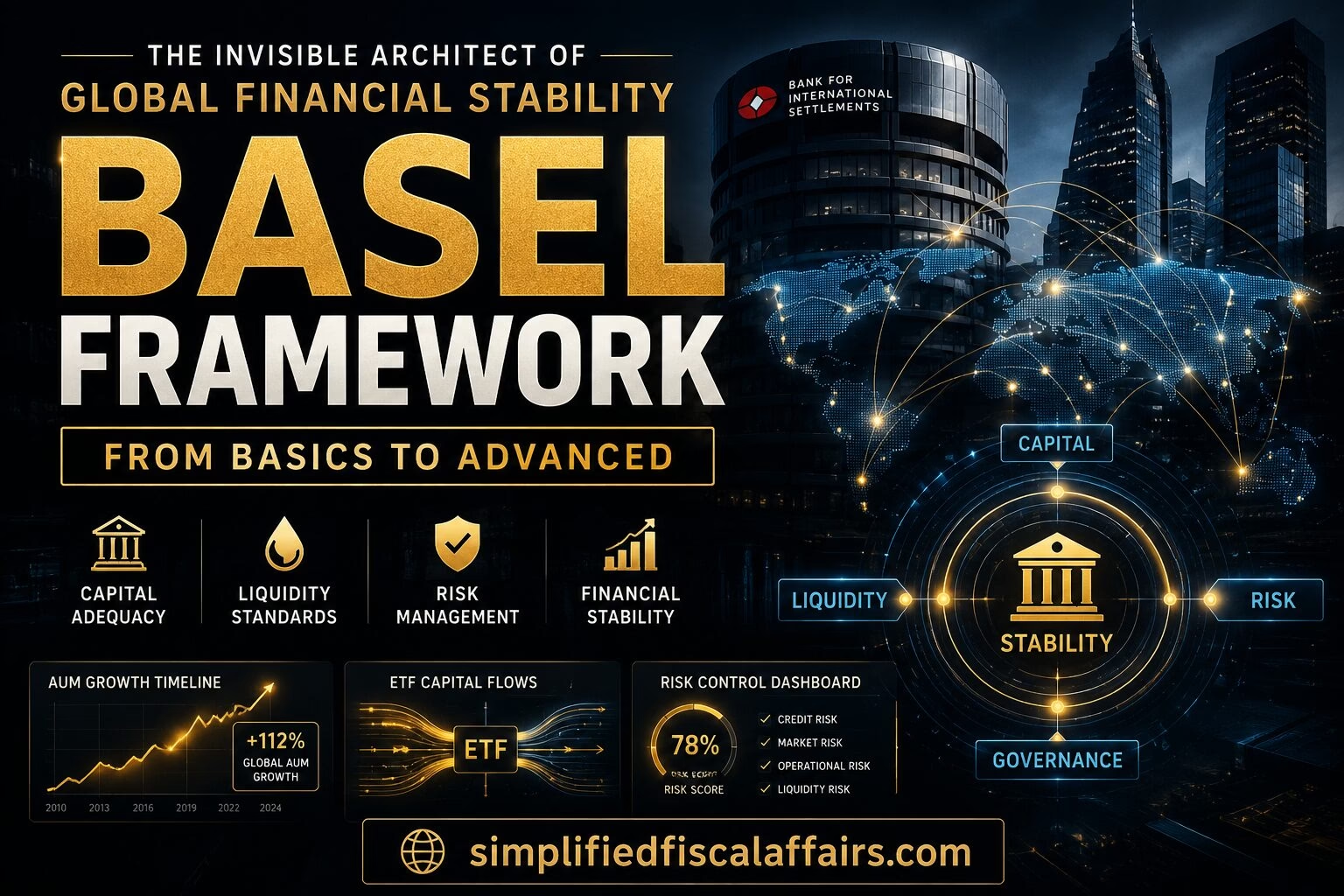

1. Introduction to the Basel Framework

The Basel Framework is a globally recognized set of banking regulations developed to strengthen financial system stability by ensuring that banks maintain adequate capital and manage risks prudently.

It is issued by the Basel Committee on Banking Supervision (BCBS), which operates under the Bank for International Settlements (BIS).

Why Basel Exists

Before Basel, banks operated with inconsistent capital standards across countries. This created:

- Uneven competition

- Weak risk controls

- Systemic vulnerability

The need for a unified global framework became evident after major financial disruptions like the Latin American debt crisis (1980s) and later the Global Financial Crisis 2008.

2. Evolution of the Basel Framework

2.1 Basel I (1988): The Beginning

The first Basel Accord introduced a minimum capital adequacy ratio (CAR).

Key Features:

- Minimum Capital Requirement: 8% of Risk-Weighted Assets (RWA)

- Focus: Credit Risk only

- Simple risk categorization (0%, 20%, 50%, 100%)

Limitations:

- Ignored market and operational risks

- Oversimplified risk weights

2.2 Basel II (2004): Risk Sensitivity & Sophistication

Basel II introduced a more refined approach with Three Pillars:

Pillar 1: Minimum Capital Requirements

Covers:

- Credit Risk

- Market Risk

- Operational Risk

Pillar 2: Supervisory Review

- Regulators evaluate bank risk management systems

- Focus on ICAAP (Internal Capital Adequacy Assessment Process)

Pillar 3: Market Discipline

- Increased transparency

- Mandatory disclosures

Approaches under Basel II:

- Standardized Approach

- Internal Ratings-Based (IRB) Approach

Weaknesses:

- Over-reliance on internal models

- Failed to predict systemic risks leading to 2008 crisis

2.3 Basel III (2010–Present): Strengthening the System

Basel III emerged as a response to the 2008 crisis.

Key Objectives:

- Improve capital quality

- Enhance liquidity

- Reduce systemic risk

3. Core Components of Basel III

3.1 Capital Structure

Capital is classified into:

Tier 1 Capital (Core Capital)

- Common Equity Tier 1 (CET1)

- Retained earnings

Tier 2 Capital

- Subordinated debt

- Hybrid instruments

3.2 Capital Adequacy Ratio (CAR)

Basel III Requirements:

- Minimum CAR: 8%

- CET1: 4.5%

- Capital Conservation Buffer: 2.5%

- Total Requirement: ~10.5%

3.3 Leverage Ratio

Controls excessive borrowing:

- Minimum: 3%

3.4 Liquidity Standards

Liquidity Coverage Ratio (LCR)

- Ensures short-term liquidity survival

Net Stable Funding Ratio (NSFR)

- Promotes long-term funding stability

3.5 Capital Buffers

A capital buffer is mandatory extra capital that banks must hold above minimum regulatory requirements, acting as a financial cushion to absorb losses during economic stress. It is established under the Basel III framework to protect depositors by mandating banks to maintain capital during prosperous times to use during econic slowdowns

Types:

- Capital Conservation Buffer (CCB)

- Countercyclical Buffer (CCyB)

- Systemically Important Bank Buffer (SIBs)

4. Risk Types Covered

4.1 Credit Risk

Risk of borrower default

4.2 Market Risk

Loss due to market fluctuations (interest rates, FX, equity)

4.3 Operational Risk

Loss due to:

- System failures

- Fraud

- Human error

5. Risk-Weighted Assets (RWA)

RWA is the backbone of Basel:

Example:

- Government bonds → 0%

- Corporate loans → 100%

6. Advanced Concepts in Basel III

6.1 Stress Testing

Banks simulate crisis scenarios:

- Economic downturn

- Market crash

Purpose: Ensure capital resilience

6.2 Systemically Important Banks (SIBs)

Large banks whose failure can disrupt the system:

- Global SIBs (G-SIBs)

- Domestic SIBs (D-SIBs)

They must maintain higher capital buffers.

6.3 Too Big to Fail (TBTF) Problem

Basel III attempts to reduce reliance on government bailouts by strengthening:

- Capital

- Resolution frameworks

6.4 Basel III Final Reforms (Basel IV)

Though unofficially called Basel IV, it includes:

- Output Floor (limits internal model benefits)

- Revised standardized approaches

- Enhanced risk measurement

7. Practical Example (Banking Scenario)

Consider a bank:

- Total Capital = ₹1,000 crore

- RWA = ₹8,000 crore

CAR = 12.5% → Above Basel requirement

However:

- If risky loans increase → RWA rises

- CAR falls → Bank must raise capital

8. Basel Framework in India

In India, Basel norms are implemented by the Reserve Bank of India (RBI).

Key Points:

- Indian banks follow Basel III norms

- Stricter capital requirements than global standards

- Regular stress testing by RBI

9. Advantages of the Basel Framework

- Enhances financial stability

- Promotes risk awareness

- Improves investor confidence

- Standardizes global banking practices

10. Criticisms and Challenges

- Complex implementation

- High compliance cost

- Over-reliance on models (Basel II issue)

- May restrict lending during downturns

11. Future of Basel Framework

The future focuses on:

- Climate risk integration

- Digital banking risks

- Fintech regulation

- Cyber risk frameworks

12. Conclusion

The Basel Framework has evolved from a simple capital rule (Basel I) to a sophisticated global risk management system (Basel III). It balances financial stability, risk sensitivity and economic growth, though challenges remain in implementation and adaptability.

Bonus: Viva Questions & Answers

Q1. What is Basel III?

A: A regulatory framework to strengthen bank capital, liquidity and risk management.

Q2. What is CAR?

A: Ratio of bank capital to risk-weighted assets.

Q3. Difference between LCR and NSFR?

A: LCR = short-term liquidity; NSFR = long-term stability.

Q4. What are RWAs?

A: Assets weighted based on risk level.

Q5. Who implements Basel in India?

A: RBI.

Case Study: Basel III Implementation – State Bank of India (SBI)

1. Background of the Bank

- Established: 1955

- Type: Public Sector Bank

- Regulator: Reserve Bank of India

- Status: Domestic Systemically Important Bank (D-SIB)

SBI is a strong example because:

- It follows Basel III norms strictly

- It publishes detailed disclosures (Pillar 3 reports)

2. Financial Snapshot (Recent Real Data Approximation)

(Based on FY 2023–24 annual report trends)

| Metric | Value |

|---|---|

| Total Assets | ₹55+ lakh crore |

| Total Capital | ~₹4.5 lakh crore |

| Risk Weighted Assets (RWA) | ~₹30 lakh crore |

| Net Profit | ₹60,000+ crore |

| Gross NPA | ~2.2% |

3. Capital Adequacy Analysis (Basel III)

Step 1: CAR Calculation

SBI Data Application:

- Total Capital = ₹4.5 lakh crore

- RWA = ₹30 lakh crore

CAR = 15% (approx.)

Interpretation:

- Basel requirement: 10.5%

- SBI: ~15% → Strong capital buffer

4. Capital Structure Breakdown

| Component | Ratio |

|---|---|

| CET1 Ratio | ~10.5% |

| Tier 1 Ratio | ~12.5% |

| Total Capital Ratio | ~15% |

Insight:

- High CET1 indicates strong core capital quality

- Lower dependence on risky hybrid instruments

5. Risk-Weighted Assets (RWA) Composition

| Risk Type | Share |

|---|---|

| Credit Risk | ~85% |

| Market Risk | ~5% |

| Operational Risk | ~10% |

Analysis:

- Heavy reliance on lending → Credit risk dominant

- Reflects traditional banking model

6. Liquidity Position (Basel III Compliance)

Liquidity Coverage Ratio (LCR)

- SBI LCR: ~130–150%

- Basel Requirement: 100%

Interpretation:

- Strong ability to survive 30-day stress scenario

Net Stable Funding Ratio (NSFR)

- SBI NSFR: ~120%+

Interpretation:

- Stable long-term funding profile

7. Leverage Ratio Analysis

- SBI Leverage Ratio: ~6%

- Basel Minimum: 3%

Insight:

- Low excessive leverage risk

- Strong solvency position

8. Stress Testing Scenario (Practical Insight)

Scenario: Economic Slowdown

Assume:

- Increase in NPAs

- Loan defaults rise

Impact:

- RWA increases

- Capital reduces

Example:

| Metric | Before | After Stress |

|---|---|---|

| Capital | ₹4.5 lakh cr | ₹4.2 lakh cr |

| RWA | ₹30 lakh cr | ₹32 lakh cr |

| CAR | 15% | 13.1% |

Conclusion:

- Still above Basel requirement → Resilient bank

9. Systemically Important Bank (D-SIB) Impact

SBI is classified as a Domestic Systemically Important Bank.

Additional Requirement:

- Extra capital buffer (~0.6–0.8%)

Reason:

- Failure could impact entire Indian economy

10. Key Basel III Strengths Observed

✔ Strong capital adequacy

✔ High liquidity buffers

✔ Controlled leverage

✔ Reduced NPAs (improved asset quality)

11. Challenges Faced

- Managing large credit portfolio risk

- Balancing profitability vs capital requirements

- Compliance cost of Basel norms

- Exposure to macroeconomic cycles

12. Strategic Actions Taken by SBI

- Improved credit appraisal systems

- Digital risk monitoring

- Reduction in bad loans

- Capital raising via equity markets

13. Comparative Insight (Global Context)

Compared to global banks:

- SBI capital levels are conservative

- Indian regulation (RBI) is stricter than Basel minimums

14. Key Learning from Case Study

This case demonstrates:

👉 Basel III is not just regulatory—it is strategic risk management

👉 Strong capital = shock absorption capacity

👉 Liquidity standards = survival in crisis

👉 Stress testing = forward-looking stability

15. Conclusion

The case of SBI shows that effective Basel III implementation leads to:

- Financial resilience

- Strong investor confidence

- Sustainable banking operations

It also highlights how regulatory discipline can transform a large public sector bank into a globally stable institution.

Bonus Viva Questions (Case-Based)

Q1. Why is SBI considered safe under Basel III?

A: High CAR, strong CET1, and liquidity ratios above Basel norms.

Q2. What happens if SBI’s RWA increase?

A: CAR falls, requiring capital infusion.

Q3. Why does SBI need extra capital buffer?

A: Because it is a D-SIB.

Q4. What is the biggest risk for SBI?

A: Credit risk due to large loan portfolio.