Corporate finance is the backbone of business operations, encompassing financial planning, decision-making and risk management.

Effective corporate finance is crucial for business success, driving growth, profitability and sustainability.

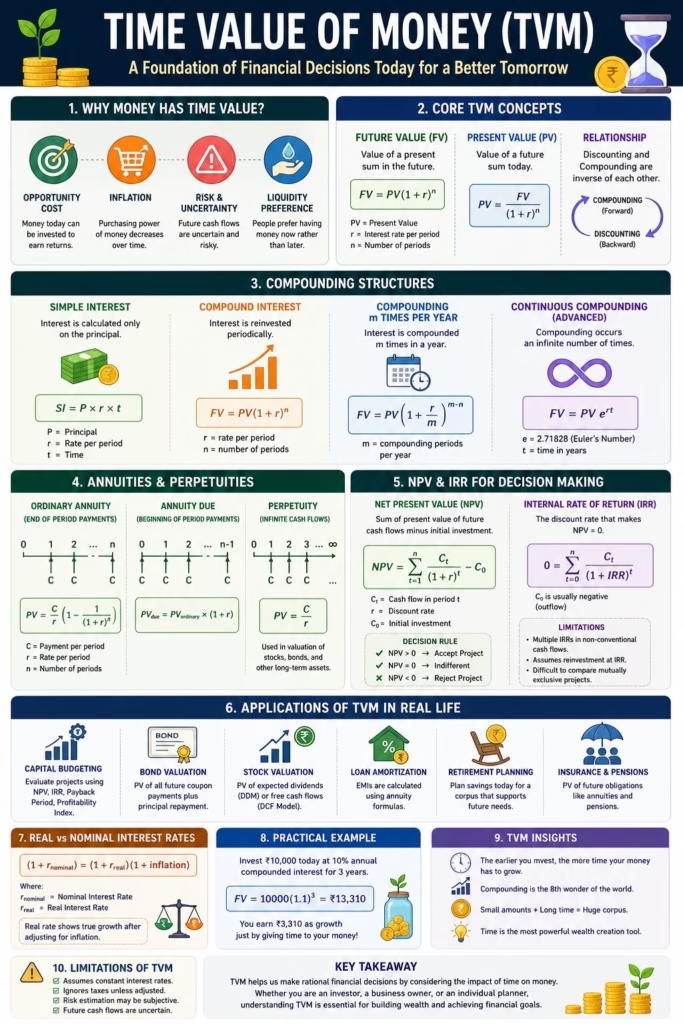

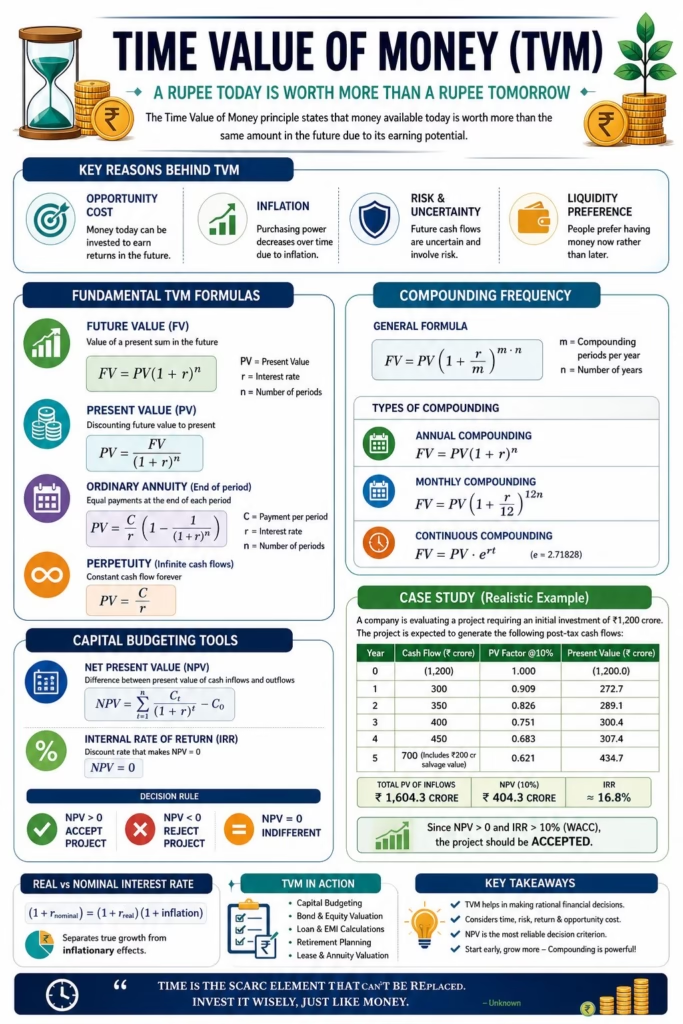

The Time Value of Money (TVM) is a foundational concept in finance that asserts a simple but powerful idea: a rupee today is worth more than a rupee in the future. This principle arises due to the potential earning capacity of money—through investment, interest, or opportunity.

At a deeper level, TVM forms the backbone of capital budgeting, valuation models, financial instruments pricing and risk assessment frameworks. Understanding TVM is essential for making rational financial decisions across corporate finance, banking, and personal investment domains.

1. Core Economic Framework Behind TVM

The value of money changes over time due to:

1. Opportunity Cost

Money today can be invested to earn returns (e.g., equity, bonds, business ventures). Delaying consumption means foregoing potential gains.

2. Inflation

Purchasing power erodes over time. ₹100 today may buy less in the future.

3. Risk and Uncertainty

Future cash flows are uncertain. Investors demand compensation (risk premium).

4. Liquidity Preference

Individuals prefer immediate availability of funds over delayed access.

2. Fundamental TVM Concepts

(a) Future Value (FV)

Future Value calculates how much a present sum will grow over time at a given interest rate.

Where:

- ( PV ) = Present Value

- ( r ) = Interest rate

- ( n ) = Number of periods

Interpretation:

FV captures compounding, where interest earns interest over time.

(b) Present Value (PV)

Present Value discounts future cash flows to today’s terms.

PV=FV /(1+r)n

Insight:

PV reflects how much a future sum is worth today given a required rate of return.

(c) Discounting vs Compounding

- Compounding: Moving forward in time

- Discounting: Moving backward in time

These are inverse processes and form the basis of valuation models.

3. Compounding Structures

(a) Simple vs Compound Interest

- Simple Interest:

SI=P×r×t - Compound Interest:

Interest is reinvested periodically, leading to exponential growth.

(b) Frequency of Compounding

The more frequent the compounding, the higher the effective return:

FV=PV(1+mr)m⋅n

[FV = PV \left(1 + \frac{r}{m}\right)^{m \cdot n}]

Where:

- ( m ) = compounding periods per year

(c) Continuous Compounding (Advanced)

[FV = PV \cdot e^{rt}]

Used in derivatives pricing and quantitative finance.

4. Annuities and Perpetuities

(a) Ordinary Annuity (End-of-period payments)

[PV = \frac{C}{r} \left(1 – \frac{1}{(1+r)^n}\right)]

(b) Annuity Due (Beginning-of-period payments)

Multiply ordinary annuity by ( (1 + r) )

(c) Perpetuity (Infinite cash flows)

[PV = \frac{C}{r}]

Application:

Used in equity valuation (Dividend Discount Model) and government bonds.

5. Net Present Value (NPV) and Decision Making

[NPV = sum \frac{C_t}/{(1+r)^t} – C_0]

Decision Rule:

- NPV > 0 → Accept project

- NPV < 0 → Reject project

Significance:

NPV integrates time, risk, and return into a single metric.

6. Internal Rate of Return (IRR)

IRR is the discount rate that makes:

[NPV = 0]

Limitations:

- Multiple IRRs in non-conventional cash flows

- Assumes reinvestment at IRR (often unrealistic)

7. Advanced Applications of TVM

(a) Capital Budgeting

- Project evaluation (NPV, IRR, Payback Period)

- Cash flow forecasting

(b) Financial Instruments Valuation

- Bonds: Present value of coupons + principal

- Stocks: Discounted dividends or free cash flows

(c) Loan Amortization

EMIs are calculated using annuity formulas.

(d) Risk-Adjusted Discounting

Discount rate includes:

- Risk-free rate

- Inflation premium

- Risk premium

8. Real vs Nominal Interest Rates

[(1 + r_{nominal}) = (1 + r_{real})(1 + inflation)]

Insight:

Separates true growth from inflationary effects.

9. Practical Example

Suppose you invest ₹10,000 at 10% for 3 years:

[FV = 10000(1.1)^3 = 13,310]

This demonstrates exponential growth due to compounding.

10. Behavioral and Strategic Insights

- Investors often undervalue long-term compounding

- Delayed investments significantly reduce wealth creation

- TVM explains why early investing is critical

11. Limitations of TVM

- Assumes constant interest rates

- Ignores taxes unless adjusted

- Risk estimation may be subjective

- Real-world cash flows are uncertain

12. Real-World Case Insight

A company evaluating a ₹5 crore project with expected returns over 5 years will:

- Forecast cash flows

- Discount them using WACC

- Compute NPV

If NPV is positive, shareholder value increases—demonstrating TVM in corporate decision-making.

Conclusion

The Time Value of Money is not just a formulaic concept—it is a philosophy of financial decision-making. It integrates time, risk, return, and opportunity cost into a unified analytical framework. Whether in investment strategy, corporate finance, or personal wealth planning, mastery of TVM enables rational, value-maximizing decisions.

📊 Case Study: Capital Investment Decision using Time Value of Money

Company Overview

Reliance Industries Limited is evaluating an investment in a new petrochemical expansion unit.

- Industry: Energy & Petrochemicals

- Decision Type: Capital Budgeting

- Investment Size: ₹1,200 crore

1. Project Details

Initial Investment (Year 0)

- Plant & Machinery: ₹900 crore

- Working Capital: ₹300 crore

👉 Total Initial Outflow = ₹1,200 crore

Expected Cash Inflows (Post-Tax)

| Year | Cash Flow (₹ crore) |

|---|---|

| 1 | 300 |

| 2 | 350 |

| 3 | 400 |

| 4 | 450 |

| 5 | 500 |

Other Assumptions

- Discount Rate (WACC): 10%

- Project Life: 5 years

- Salvage Value: ₹200 crore (included in Year 5)

2. Step-by-Step TVM Analysis

(A) Present Value of Cash Flows

Using TVM discounting:

| Year | Cash Flow | PV Factor (10%) | Present Value |

|---|---|---|---|

| 1 | 300 | 0.909 | 272.7 |

| 2 | 350 | 0.826 | 289.1 |

| 3 | 400 | 0.751 | 300.4 |

| 4 | 450 | 0.683 | 307.4 |

| 5 | 700 | 0.621 | 434.7 |

👉 Total PV of Inflows = ₹1,604.3 crore

(B) Net Present Value (NPV)

[

NPV = 1604.3 – 1200 = ₹404.3 \text{ crore}

]

✅ Decision: ACCEPT PROJECT

- Positive NPV → Value creation for shareholders

(C) Internal Rate of Return (IRR)

- IRR ≈ 16.8%

- Since IRR > WACC (10%) → Project is profitable

(D) Payback Period (Additional Insight)

- Cumulative recovery occurs between Year 3 & 4

👉 Approx. 3.2 years

3. Interpretation & Strategic Insight

Why TVM Matters Here

- ₹1,200 crore today is not comparable to future inflows without discounting

- TVM adjusts for:

- Risk

- Inflation

- Opportunity cost

Value Creation Analysis

- Project generates ~34% extra value over investment

- Strong IRR indicates efficient capital utilization

4. Sensitivity Analysis (Advanced CA-Level Insight)

| Scenario | Discount Rate | NPV (₹ crore) |

|---|---|---|

| Base Case | 10% | 404 |

| High Risk | 14% | 210 |

| Low Risk | 8% | 520 |

👉 Shows NPV sensitivity to cost of capital

5. Risk Factors

- Crude oil price volatility

- Regulatory changes

- Demand fluctuations in petrochemical sector

6. Real-World Relevance

Companies like Reliance Industries Limited, Indian Oil Corporation, and ONGC regularly use TVM techniques for:

- Refinery expansions

- Infrastructure investments

- Energy transition projects

7. Key Learning Outcomes

- TVM is essential for investment decision-making

- NPV is the most reliable method

- IRR provides return perspective but has limitations

- Real-world decisions require risk-adjusted discounting

8. Conclusion

This case clearly demonstrates how Time Value of Money transforms raw financial data into meaningful insights. Without TVM, the project might appear profitable—but only through discounting can we confirm true economic value creation.

TIME IS THE SCARCE ELEMENT THAT CAN'T BE REPLACED, INVEST IT WISELY, JUST LIKE MONEY.