WHAT IS AUDIT?

“Audit is an examination of accounting records, undertaken with a view to establishing whether they correctly and completely reflect the transactions to which they purport to relate.” Prof. Dickers

“Auditing is concerned with the verification of accounting data, determining the accuracy and reliability of accounting statements and reports.” R.R. Mautz

“Long range objectives of an Audit should be to serve as a guide to management's future decisions in all financial matters such as controlling, forecasting, analysing and reporting. These objectives help the business unit to improve its performance.” Arthur W. Holme

- Auditing is nothing but the systematic and critical examination and verification of the books of accounts. It can be undertaken throughout the year or periodically.

- The primary aim is to find out whether the financial statements exhibit a true and fair view of the business.

- Origin of the term audit is said to be in the Latin term audire which means to listen.

- Audit of accounts by a duty qualified chartered accountant is mandatory for the registered joint stock companies, public trusts, bigger co-operative societies and for income tax and VAT tax payers above a particular limit.

Objectives of Audit:

- To find the reliability of the financial position and profit and loss statement.

- To check whether the financial statements of the company present a true and fair view.

- To check whether the financial statements are kept as per the provisions of the relevant Act.

- Verification of the entries with the relevant documentary evidences.

- To check whether all the money received is accounted for or not and all the payments made have proper supporting documents.

- To conduct an independent review of financial statements.

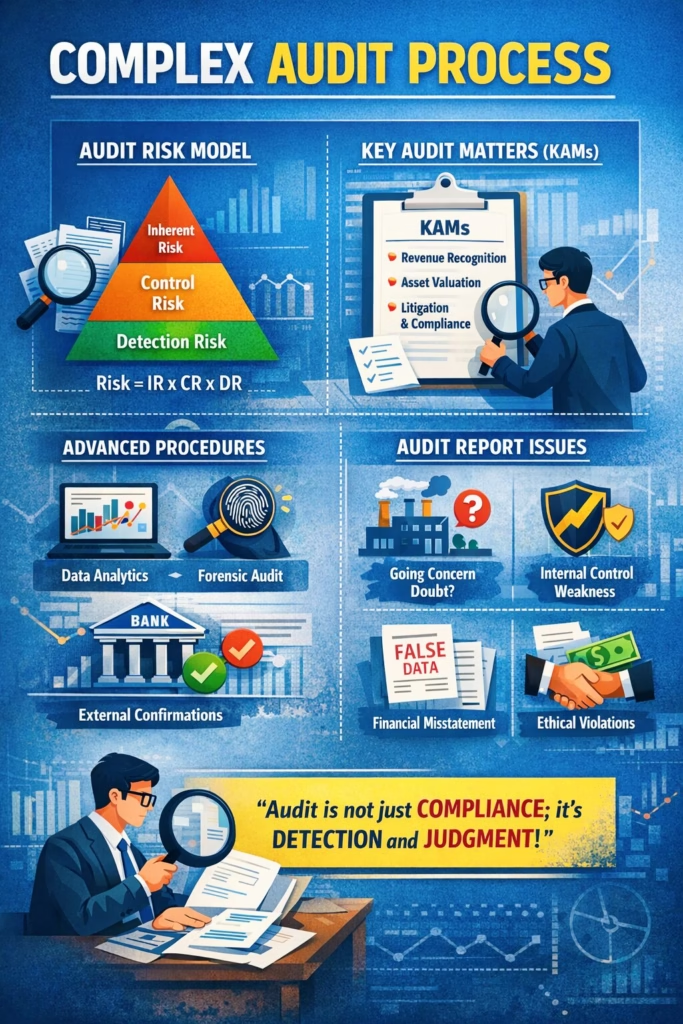

- Auditor has to examine the prevailing internal control and internal check systems prevalent in the organisation and must check the arithmetical accuracy of the books of accounts.

- The auditor has to check the physical existence of various assets shown in the balance sheet and check whether they present a true and fair value.

- After checking the accounts the auditor has to express his or her personal judgement on the maintenance of the books of accounts.

- The company who audits its financial statements on a timely basis builds a good reputation and goodwill.

- Helps the stakeholders with decision making as audited accounts are considered more reliable.

- To detect and prevent frauds and errors.

The main difference between the two (frauds and errors) is that errors are generally committed due to lack of knowledge and are considered to be innocent, whereas, frauds are committed intentionally.

HOW AUDITORS DETECT FRAUD?

The Hidden Methods Behind Billion-Dollar Financial Scandals

Introduction — Why Fraud Keeps Happening

From the collapse of Enron to the downfall of Wirecard and the massive deception behind Luckin Coffee, history repeatedly shows that corporations can manipulate financial statements for years before anyone notices.

But eventually, auditors begin seeing something unusual.

The numbers stop making sense.

Margins rise too perfectly.

Cash flows contradict profits.

Executives become defensive.

And somewhere inside thousands of transactions, hidden evidence begins to emerge.

Modern auditing is no longer just “checking invoices.”

It is a sophisticated mix of:

- Financial intelligence

- Data analytics

- Behavioral psychology

- Statistical analysis

- Investigative interviewing

- Digital forensic testing

Auditors today operate like financial detectives.

Their job is not merely to confirm numbers.

Their job is to identify whether the story management tells investors is actually true.

WHAT IS FRAUD IN AUDITING?

Fraud refers to an intentional act designed to deceive users of financial statements.

Auditors primarily focus on two categories:

1. Fraudulent Financial Reporting

This occurs when companies manipulate accounting records to appear healthier than reality.

Examples include:

- Fake revenue recognition

- Inflated profits

- Hidden liabilities

- Overstated assets

- Understated expenses

Famous Examples

| Company | Fraud Type | Estimated Impact |

|---|---|---|

| Enron | Hidden debt entities | $74 Billion collapse |

| Wirecard | Fake cash balances | €1.9 Billion missing |

| Satyam | Inflated revenue | ₹7,000+ Crore scandal |

| Luckin Coffee | Fabricated sales | $300M+ fake transactions |

2. Misappropriation of Assets

This involves theft or misuse of company resources.

Examples:

- Employee embezzlement

- Payroll fraud

- Fake vendor payments

- Inventory theft

- Expense reimbursement fraud

While smaller individually, these frauds collectively cost businesses billions annually.

THE FRAUD TRIANGLE — WHY PEOPLE COMMIT FRAUD

One of the most important concepts in auditing is the Fraud Triangle.

The Fraud Triangle explains that fraud usually occurs when three conditions exist simultaneously:

1. Pressure

Financial or personal stress pushes individuals toward unethical behavior.

Examples:

- Debt

- Bonus targets

- Stock market expectations

- Job insecurity

2. Opportunity

Weak internal controls create openings for manipulation.

Examples:

- Poor oversight

- Lack of segregation of duties

- Weak approval systems

- Ineffective audit committees

3. Rationalization

Fraudsters justify their actions psychologically.

Common thinking patterns include:

- “I deserve this.”

- “I’ll repay it later.”

- “The company owes me.”

Auditors carefully evaluate all three elements when assessing fraud risk.

PROFESSIONAL SKEPTICISM — THE AUDITOR’S MOST POWERFUL WEAPON

Professional skepticism means maintaining a questioning mindset throughout the audit.

It requires auditors to:

- Challenge unusual explanations

- Verify management claims independently

- Investigate inconsistencies

- Assume material misstatement could exist

A skeptical auditor does not simply trust documents because management provides them.

Instead, they ask:

- Why are margins unusually high?

- Why are revenues rising while cash flows decline?

- Why are confirmations delayed?

- Why do related-party transactions look abnormal?

Professional skepticism often separates successful fraud detection from catastrophic audit failure.

ANALYTICAL PROCEDURES — FINDING THE HIDDEN PATTERNS

Analytical procedures involve studying relationships within financial data to identify abnormalities.

Auditors compare:

- Current vs prior year performance

- Industry averages

- Competitor benchmarks

- Operational metrics

- Seasonal trends

When numbers behave unusually, fraud risk increases.

Example — Revenue Manipulation

Suppose a company reports:

- Revenue growth: +40%

- Cash flow growth: +2%

This mismatch becomes suspicious.

If sales are real, cash collections should generally increase as well.

Such inconsistencies often trigger deeper investigation.

RATIO ANALYSIS — DETECTING FINANCIAL DISTORTIONS

Ratio analysis helps auditors identify manipulation hidden inside financial statements.

Key ratios include:

Profitability Ratios

- Gross Profit Margin

- Operating Margin

- Net Profit Margin

Sudden unexplained improvements may indicate earnings manipulation.

Liquidity Ratios

- Current Ratio

- Quick Ratio

- Cash Ratio

Weak liquidity despite strong profits can indicate fake revenue.

Efficiency Ratios

- Inventory Turnover

- Receivable Turnover

- Asset Utilization

Abnormal receivable growth may suggest fictitious sales.

Leverage Ratios

- Debt-to-Equity

- Interest Coverage

Hidden liabilities often distort leverage patterns.

CONFIRMATION TESTING — VERIFYING THE TRUTH DIRECTLY

Confirmation testing is one of the strongest forms of audit evidence.

Auditors independently contact third parties to verify:

- Bank balances

- Customer receivables

- Supplier balances

- Legal claims

- Loan obligations

This is critical because fraudsters can manipulate internal records, but external confirmations are harder to fake.

Why Confirmation Testing Matters

In the Wirecard scandal, billions of euros supposedly held in trustee bank accounts never actually existed.

Independent verification exposed the deception.

This demonstrates a fundamental audit principle:

“Trust, but verify independently.”

TRANSACTION TRACING — FOLLOWING THE MONEY

Transaction tracing means tracking transactions from origin to final recording.

Auditors examine:

- Invoices

- Contracts

- Shipping documents

- Payment approvals

- Bank statements

- ERP system logs

The goal is to determine whether transactions are:

- Genuine

- Authorized

- Properly recorded

- Supported by evidence

Red Flags During Transaction Tracing

Auditors become suspicious when they find:

- Round-dollar transactions

- Duplicate invoices

- Missing documentation

- Backdated contracts

- Unusual journal entries

- Transactions near year-end

These are common indicators of financial manipulation.

INTERVIEW TECHNIQUES — DETECTING BEHAVIORAL CLUES

Fraud detection is not only about numbers.

Human behavior often reveals hidden risks.

Experienced auditors conduct strategic interviews with:

- Management

- Employees

- Vendors

- Internal auditors

- Operational staff

Behavioral Red Flags

Auditors pay attention to:

- Defensive responses

- Inconsistent explanations

- Excessive detail

- Nervous behavior

- Avoidance of direct questions

Sometimes the biggest clue is not the accounting entry.

It is the reaction when someone is questioned about it.

AUDIT EVIDENCE — BUILDING THE CASE

Audit evidence forms the foundation of fraud detection.

High-quality evidence must be:

- Sufficient

- Reliable

- Relevant

- Independent

Auditors prefer external evidence because it is harder to manipulate.

Examples include:

- Bank confirmations

- Tax filings

- Customer confirmations

- Legal documents

- Third-party contracts

Weak or contradictory evidence increases audit risk significantly.

TECHNOLOGY & MODERN FRAUD DETECTION

Today’s auditors increasingly use:

AI-Based Analytics

Artificial intelligence can identify anomalies across millions of transactions instantly.

Continuous Monitoring

Automated systems monitor transactions in real time.

Benford’s Law Analysis

Benford’s Law identifies unnatural number distributions that may indicate manipulation.

ERP Forensics

Auditors analyze system logs to detect:

- Unauthorized access

- Manual overrides

- Suspicious entries

- Deleted records

CASE STUDY — HOW ENRON FOOLED THE WORLD

Enron used complex off-balance-sheet entities to hide debt and inflate profitability.

Red flags included:

- Extremely complex structures

- Unrealistic profit margins

- Weak transparency

- Aggressive accounting assumptions

Eventually:

- Investors lost billions

- Thousands lost jobs

- Auditor credibility collapsed

- Global audit regulations changed permanently

The scandal directly influenced the creation of the Sarbanes-Oxley Act (SOX), which strengthened internal controls and auditor independence.

WHY SOME FRAUDS STILL GO UNDETECTED

Despite advanced audit techniques, fraud may remain hidden because:

- Management overrides controls

- Collusion bypasses systems

- Evidence is falsified

- Audits rely on sampling

- Fraudsters exploit complexity

This is why auditing provides “reasonable assurance,” not absolute certainty.

THE FUTURE OF FRAUD DETECTION

The future of auditing will increasingly involve:

- Artificial intelligence

- Predictive fraud analytics

- Blockchain verification

- Continuous auditing

- Real-time transaction testing

Future auditors may analyze entire populations of transactions rather than small samples.

This could fundamentally transform fraud detection accuracy.

FINAL THOUGHTS — THE WAR BETWEEN TRUTH & DECEPTION

Fraud detection is ultimately a battle between:

- Transparency and manipulation

- Evidence and deception

- Skepticism and blind trust

Auditors serve as financial gatekeepers protecting:

- Investors

- Banks

- Pension funds

- Employees

- Capital markets

Every major fraud leaves behind clues.

The challenge is whether auditors identify those clues before billions disappear.

And in a world increasingly driven by complex financial systems, the ability to detect fraud has never been more important.

QUICK SUMMARY TABLE

| Audit Method | Purpose | Fraud Indicator |

|---|---|---|

| Analytical Procedures | Detect abnormal trends | Unusual fluctuations |

| Ratio Analysis | Identify distortions | Margin inconsistencies |

| Confirmation Testing | Verify external balances | Fake assets/liabilities |

| Transaction Tracing | Validate transactions | Unsupported entries |

| Interview Techniques | Detect behavioral clues | Evasive responses |

| Professional Skepticism | Challenge assumptions | Hidden manipulation |