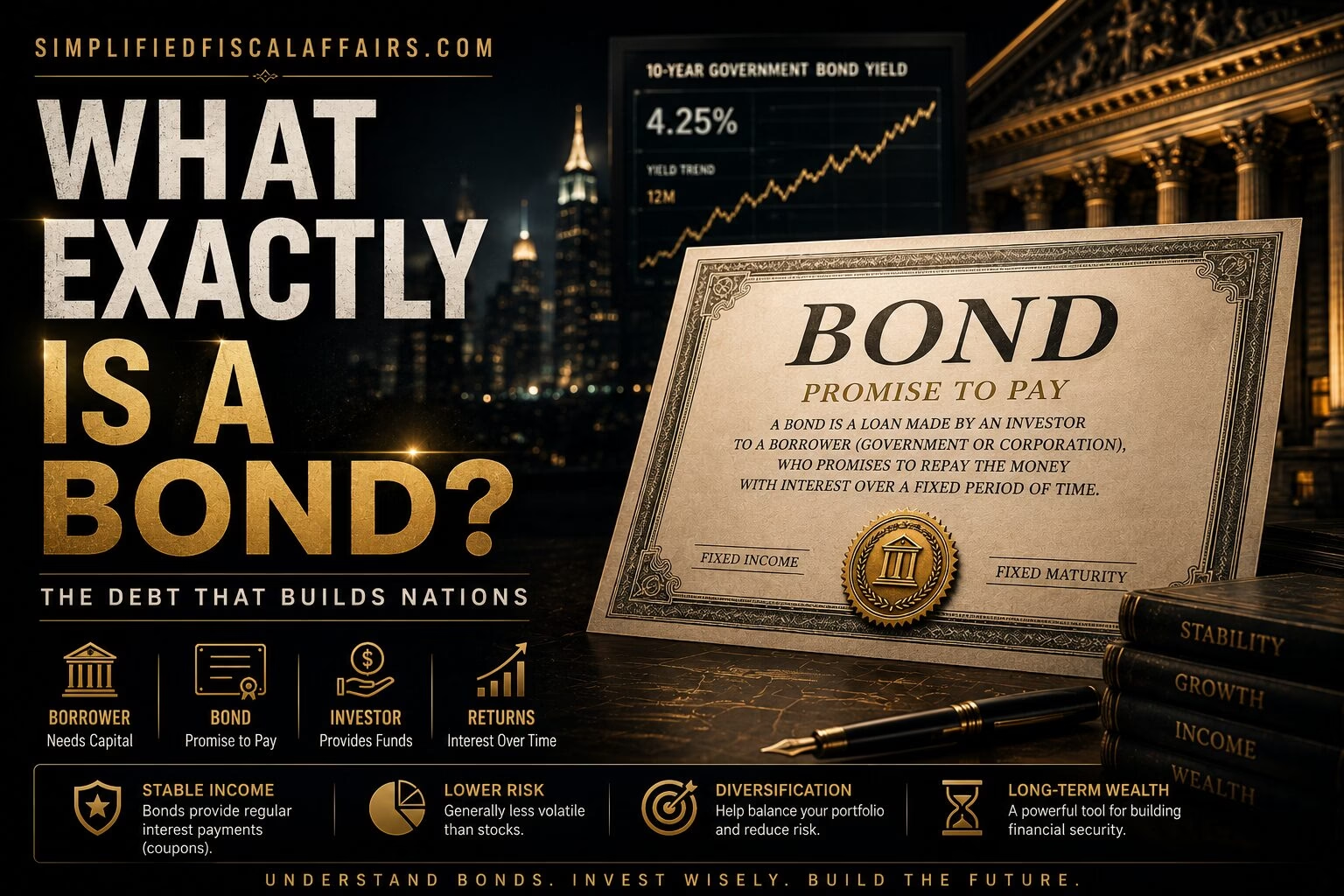

SERIES 2 – What Exactly Is a Bond?

Understanding the World’s Simplest Financial Promise

“Every bond begins with a simple promise: ‘Lend me money today, and I’ll repay you tomorrow—with interest.'”

Introduction

If the global bond market is worth more than $100 trillion, one question naturally follows:

What exactly is a bond?

You may have heard financial news anchors say things like:

- “Government bond yields are rising.”

- “Corporate bond issuance reached record levels.”

- “Investors are moving from stocks to bonds.”

- “Treasury bonds are considered safe-haven assets.”

These statements can sound intimidating, but the underlying concept is surprisingly simple.

At its heart, a bond is nothing more than a formal loan agreement.

Unlike a casual loan between friends or family, a bond is a legally enforceable financial contract. It specifies exactly how much money has been borrowed, how much interest will be paid, when repayments will occur, and when the loan must be fully repaid.

Understanding this single idea unlocks much of the modern financial system.

Imagine Becoming the Bank

Suppose your friend wants to start a coffee shop.

The business requires ₹10 lakh, but your friend doesn’t want to sell part of the business to investors.

Instead, they ask you for a loan.

You agree to lend the money under these conditions:

- Loan Amount: ₹10,00,000

- Interest Rate: 8% per year

- Loan Duration: 10 years

- Interest paid every year

- Full repayment after 10 years

Instead of shaking hands, both of you sign a legal agreement.

That agreement is essentially a bond.

You have become the lender.

Your friend has become the borrower.

A Bond Is Different From Buying Shares

Many beginners confuse bonds with stocks.

Although both are financial investments, they represent completely different relationships.

When you purchase shares of a company, you become one of its owners.

If the company performs well, the value of your shares may rise. If it struggles, the value may fall dramatically.

There is no guarantee of profits.

A bond works differently.

When you purchase a bond, you do not become an owner.

Instead, you become a creditor.

You are lending money—not buying ownership.

The borrower promises to repay your money according to predetermined terms.

This distinction explains why bonds are generally considered more predictable than stocks, though they are not entirely risk-free.

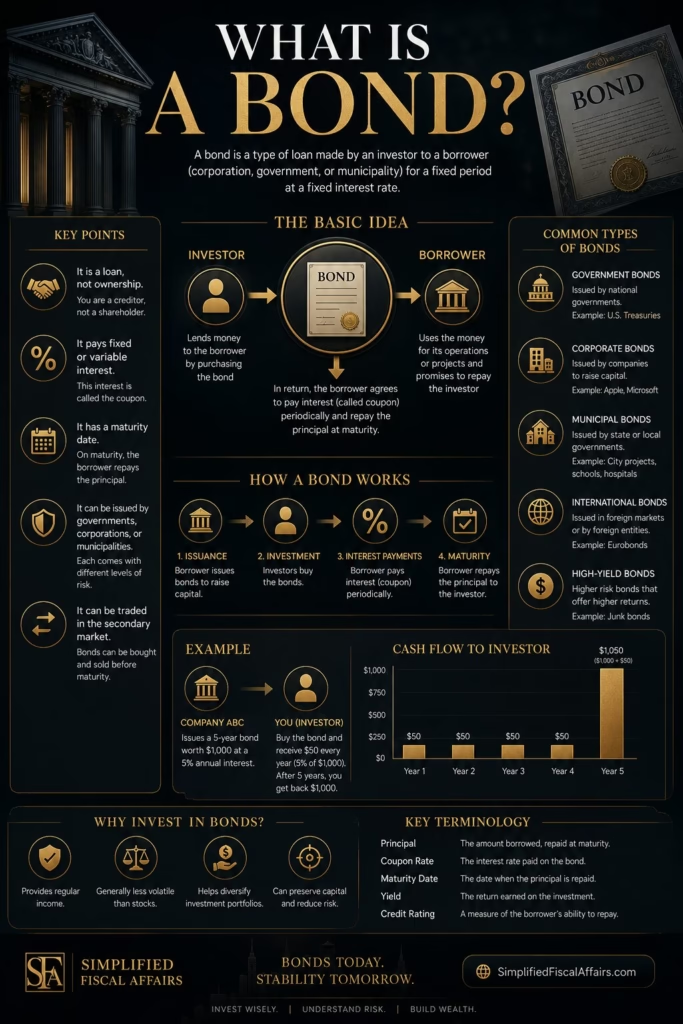

Every Bond Contains Six Essential Elements

Think of every bond as a financial identity card.

Regardless of whether it is issued by a government or a corporation, every bond includes several core components.

1. Face Value (Principal)

The face value is the amount that will be repaid when the bond reaches maturity.

For example:

Face Value = ₹1,00,000

This means that when the bond expires, the issuer promises to repay ₹1,00,000.

It is the foundation upon which all interest calculations are made.

2. Coupon Rate

The coupon rate is the annual interest paid on the bond.

Suppose the coupon rate is:

8%

If the face value is:

₹1,00,000

The investor receives:

₹8,000 every year.

This payment continues until maturity.

Some bonds distribute interest annually.

Others pay semi-annually, quarterly, or even monthly.

Regardless of frequency, the coupon represents the compensation investors receive for lending money.

3. Maturity Date

Every bond has an ending date.

This is called maturity.

At maturity:

- Interest payments stop.

- The original principal is returned.

- The legal obligation is fulfilled.

Maturities vary enormously.

Some bonds mature within a year.

Others remain outstanding for:

- 5 years

- 10 years

- 20 years

- 30 years

Certain governments have even issued bonds with maturities approaching 100 years.

4. Issuer

The issuer is the borrower.

Possible issuers include:

- National governments

- State governments

- Municipal authorities

- Banks

- Corporations

- International organizations

The reputation and financial strength of the issuer largely determine how risky a bond is perceived to be.

5. Bond Price

Many beginners assume bonds always trade at their face value.

In reality, bonds are bought and sold every day in financial markets.

As a result, their prices fluctuate.

A bond with a face value of ₹1,00,000 might trade for:

₹98,000

₹1,05,000

₹1,12,000

The reason behind these price changes will become one of the most important concepts in later series when we explore the relationship between prices and interest rates.

6. Yield

Yield represents the actual return an investor earns based on the current market price.

This differs from the coupon rate.

Imagine purchasing an existing bond at a discount.

You still receive the same coupon payments, but because you paid less than face value, your effective return becomes higher.

Yield helps investors compare bonds with different prices, maturities, and coupon rates.

Professional investors focus far more on yield than coupon rate.

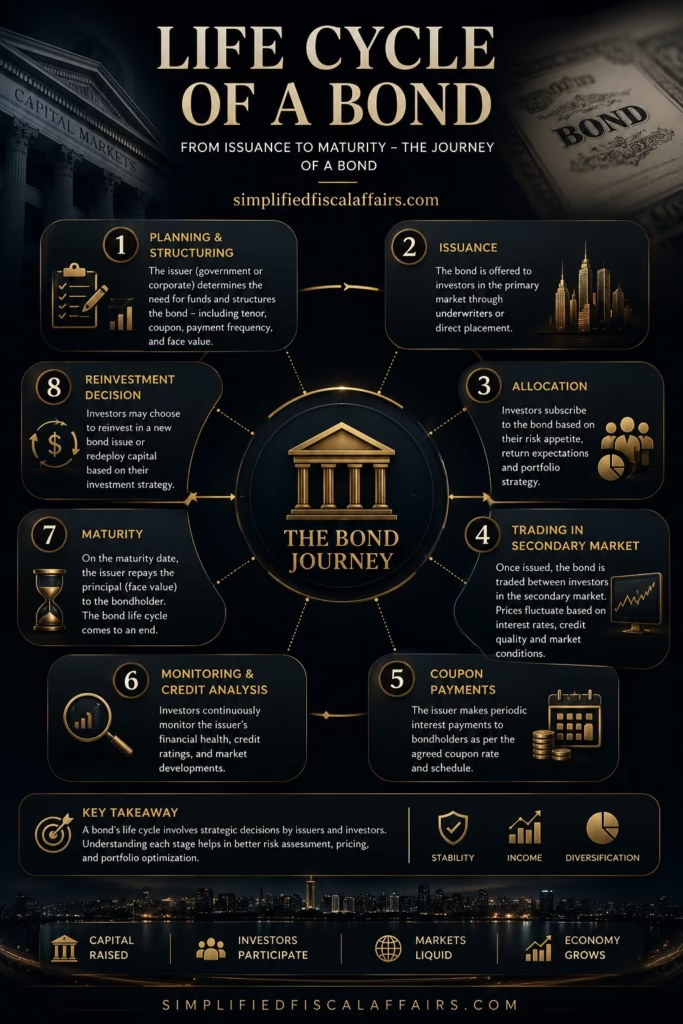

The Life Cycle of a Bond

Every bond follows a simple journey.

Step 1: Issue

A government or corporation requires funding.

It creates bonds and offers them to investors.

Step 2: Purchase

Investors lend money by purchasing those bonds.

The issuer immediately receives the capital.

Step 3: Interest Payments

Throughout the life of the bond, the issuer pays regular interest to investors.

These predictable payments make bonds attractive for institutions seeking stable income.

Step 4: Trading

Investors are not required to hold bonds until maturity.

They may sell them in secondary markets.

New investors purchase the bonds, and ownership changes while the issuer continues making payments according to the original terms.

Step 5: Maturity

On the maturity date:

- Final interest payment is made.

- Principal is repaid.

- The bond ceases to exist.

Its contractual obligations have been fulfilled.

Why Investors Buy Bonds

People often ask:

“If stocks usually generate higher returns, why do investors buy bonds?”

The answer depends on an investor’s objectives.

Many investors prioritize stability over maximum growth.

Large institutions such as pension funds and insurance companies need predictable cash flows to meet future obligations.

Governments, universities, charities, and endowment funds also rely on bonds to preserve capital while earning income.

For retirees, bonds can provide a steadier stream of interest payments than more volatile investments.

Rather than replacing stocks, bonds often complement them by helping balance risk and return within a diversified portfolio.

A Simple Analogy

Imagine the global financial system as a city.

Stocks represent ownership of the city’s businesses.

Bonds represent the loans that financed the construction of those businesses, the roads connecting them, the airports serving them, and the public infrastructure supporting economic activity.

Ownership drives innovation.

Debt provides the capital that allows growth to happen.

Both are essential, but they serve different purposes.

Key Takeaways

A bond is fundamentally a contractual promise between a borrower and a lender.

Every bond includes six key features:

- Face value

- Coupon rate

- Maturity date

- Issuer

- Market price

- Yield

Understanding these building blocks is essential before exploring more advanced topics such as bond pricing, duration, credit risk, and yield curves.

In the next series, we will travel back thousands of years to discover an unexpected truth:

Long before modern banks existed, ancient civilizations were already borrowing, lending, and recording debt. The story of bonds begins not on Wall Street, but in the earliest cities of human history.

← Previous Chapter The Invisible Giant: Understanding the $100 Trillion Bond Market – I

Next Chapter →The Birth of Debt- III

Series 3 – The Birth of Debt

How Ancient Civilizations Invented Borrowing Thousands of Years Before Modern Banks

“Long before skyscrapers, stock exchanges, and investment banks existed, humanity had already discovered one of its most powerful financial inventions—the ability to borrow from tomorrow to build today.”