“The Tricks Companies Use to Look More Profitable”

“In the world of corporate finance, appearances can be manufactured, profits can be engineered, and reality can be hidden in the footnotes.”

“Markets reward growth. Executives are rewarded for growth. But that pressure can sometimes turn accounting into a dangerous game.”

“Behind every spectacular rise in profits lies a simple question: Are the numbers real?”

A company reports record profits.

The stock price jumps.

Investors celebrate.

Executives receive bonuses.

But months later, the truth emerges: many of those profits were never really there.

This is the world of earnings manipulation—where companies use accounting flexibility to make financial performance look stronger than economic reality.

What Is Earnings Manipulation?

Earnings manipulation occurs when management intentionally alters accounting choices, estimates, or timing of transactions to present a more favorable financial picture.

Unlike outright fraud, some forms of earnings management operate within accounting rules while still misleading investors.

The goal is usually to:

- Meet analyst expectations

- Avoid reporting losses

- Maintain stock prices

- Secure financing

- Increase executive compensation

- Preserve investor confidence

The result is often a gap between reported profits and actual economic performance.

Why Earnings Matter So Much

Investors, lenders, and analysts rely heavily on earnings to evaluate companies.

A small earnings miss can trigger:

- Stock price declines

- Credit rating concerns

- Negative media coverage

- Reduced investor confidence

Because of this pressure, management may be tempted to “smooth” results.

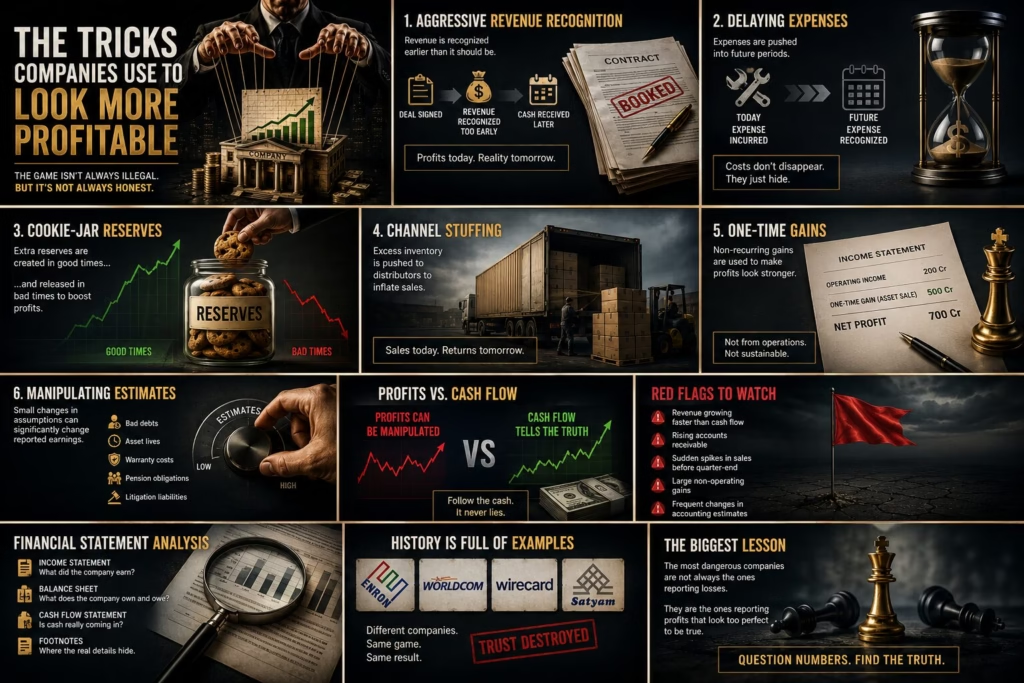

Technique 1: Aggressive Revenue Recognition

How It Works

Revenue is recognized earlier than it should be.

The company records sales before:

- Products are delivered

- Services are completed

- Customers fully commit to purchases

Example

Imagine a company signs a three-year contract worth ₹30 crore.

Instead of recognizing revenue gradually over three years, management records a large portion immediately.

Reported profits rise even though cash has not yet been earned.

Warning Signs

- Revenue growing faster than cash flow

- Large increases in receivables

- Complex revenue disclosures

- Significant year-end sales spikes

Technique 2: Delaying Expenses

How It Works

Expenses are pushed into future periods.

Current profits appear higher because costs are temporarily hidden.

Example

A company spends ₹50 crore on maintenance.

Instead of recording it as an expense today, management classifies it as an asset.

The expense disappears from the income statement, boosting profits.

Why It’s Dangerous

Eventually those costs must be recognized.

Future earnings suffer when the hidden expenses return.

Warning Signs

- Rapid asset growth

- Unusual capitalization policies

- Rising depreciation charges later

Technique 3: Cookie-Jar Reserves

How It Works

Management deliberately overestimates expenses during good years.

These excess reserves become a hidden earnings cushion.

When business slows, reserves are released to artificially boost profits.

Example

A company estimates warranty costs of ₹100 crore.

Actual expected costs are only ₹60 crore.

The extra ₹40 crore sits in reserve.

In a weak year, management reduces the reserve, creating additional profit.

Why It Misleads Investors

Profits appear stable even though business performance is fluctuating.

Warning Signs

- Frequent reserve adjustments

- Large changes in provisions

- Unusual accounting estimates

Technique 4: Channel Stuffing

How It Works

Companies push excessive inventory onto distributors near quarter-end.

Products are technically sold, allowing revenue recognition.

However, customers may not actually need the inventory.

Example

A manufacturer pressures retailers to purchase six months of inventory before year-end.

Revenue increases dramatically.

Months later, retailers stop ordering because warehouses are already full.

Future sales collapse.

Famous Problem

Many corporate accounting scandals involved channel stuffing to meet earnings targets.

Warning Signs

- Sudden sales surges before reporting periods

- Rising inventory levels at distributors

- Declining future sales growth

Technique 5: One-Time Gains Disguised as Operating Performance

How It Works

Companies sell assets and report gains.

Management highlights the profit while downplaying that it is non-recurring.

Example

A company sells land for ₹500 crore.

The gain boosts earnings.

Investors may mistakenly assume the business itself became more profitable.

Warning Signs

- Large non-operating gains

- Frequent asset sales

- Growing gap between operating income and net income

Technique 6: Manipulating Accounting Estimates

Modern accounting depends heavily on estimates.

Management estimates:

- Bad debts

- Asset lives

- Warranty costs

- Pension obligations

- Litigation liabilities

Small changes in assumptions can significantly alter earnings.

Example

Increasing an asset’s useful life from 10 years to 20 years reduces annual depreciation expense and boosts profits.

Warning Signs

- Frequent estimate revisions

- Significant management judgment disclosures

- Large swings in accounting assumptions

The Difference Between Earnings and Cash Flow

One of the best ways to detect manipulation is comparing profits with cash generation.

A company can manipulate earnings more easily than cash.

Healthy Situation

- Revenue rises

- Operating cash flow rises

Concerning Situation

- Revenue rises

- Profit rises

- Cash flow stagnates or declines

This disconnect often signals aggressive accounting.

Key Concepts Investors Should Understand

Accrual Accounting

Revenue and expenses are recognized when earned or incurred, not necessarily when cash moves.

This provides flexibility—but also creates opportunities for manipulation.

Earnings Quality

High-quality earnings are:

- Sustainable

- Supported by cash flow

- Consistent

- Transparent

Low-quality earnings rely heavily on accounting adjustments.

Financial Statement Analysis

Analysts look beyond reported profits by examining:

- Cash flow statements

- Balance sheet changes

- Revenue trends

- Expense patterns

- Accounting footnotes

The goal is to determine whether profits reflect real business performance.

Major Historical Examples

Notable corporate scandals involving earnings manipulation include:

- Enron

- WorldCom

- Wirecard

- Satyam Computer Services

These cases demonstrated how manipulated earnings can conceal serious financial problems for years.

The Bigger Lesson

Earnings manipulation rarely begins with a massive fraud.

It often starts with small accounting adjustments designed to meet expectations.

Over time, those adjustments grow larger.

Management becomes dependent on maintaining the illusion.

Eventually, economic reality catches up.

The most dangerous companies are not always the ones reporting weak profits—they may be the ones reporting profits that seem almost too perfect.

“In finance, the biggest risk isn’t always losing money. Sometimes it’s believing numbers that were designed to tell a better story than the truth.”