Introduction

In a world where billions of transactions occur every day, traditional auditing methods are increasingly challenged by the speed, complexity, and interconnected nature of modern business operations. Organizations can no longer afford to wait weeks, months, or even a full year to identify control failures, fraud risks, compliance breaches, or financial irregularities.

This evolving business environment has given rise to Continuous Audit (CA)—an advanced audit methodology that leverages automation, real-time data analytics, artificial intelligence, and continuous monitoring technologies to provide ongoing assurance over organizational processes and controls.

Continuous Audit represents a fundamental transformation in assurance practices. Rather than reviewing historical transactions after they have occurred, auditors can now monitor transactions, controls, and risks almost in real time, enabling proactive risk management and faster decision-making.

What is Continuous Audit?

- Audit that remains continue throughout the financial year is known as the continuous audit.

- The auditor checks each and every transaction. The large scale business organisations require constant check of their business transactions, as there may be declaration of dividend, during the year.

- In case of a company, where the volume of transactions is quite large, the management can follow the policy of applying continuous audit.

- If the internal control systems prevalent in the organisations are not satisfactory, then to apply continuous audit will be the best option in order to represent a true and fair view of the organisation.

Continuous Audit is a technology-enabled auditing approach in which audit-related activities are performed continuously or at frequent intervals through automated systems.

The goal is to provide:

- Real-time assurance

- Early risk detection

- Continuous control evaluation

- Automated exception reporting

- Enhanced regulatory compliance

- Faster management response

Unlike traditional audits, which are periodic and retrospective, Continuous Audit focuses on ongoing monitoring and assessment of business activities as they occur.

Definition

Continuous Audit can be defined as:

“A methodology that enables independent auditors to provide assurance simultaneously with or shortly after business events occur through the use of technology-driven automated audit procedures.”

R.G. Williams says that continuous audit is one where the auditor or his staff is consistently engaged in checking the accounts during the whole period, or where the auditor or his staff, attend at regular or irregular intervals during the period.

Advantages:

- Thorough check: The primary advantage of the continuous audit is thorough checking. The audit staff remains busy throughout the year, as each and every transaction is reviewed in detail.

- Quick detection of errors: As the auditor checks the transactions, in detail, at regular intervals there is quick detection of errors.

- Timely presentation of accounts: As most of the checking work is already performed during the year, the final audit can be presented on a timely basis to the shareholders, after the close of the financial year at the annual general meeting.

- Prompt filing of returns: The continuous audit proves beneficial for the quick filing of returns as the accounts are prepared as well as audited at the end of the year.

- Interim dividend: The continuous audit proves to be helpful for the declaration of the interim dividend.

- Moral check on the client’s staff: The continuous audit is useful to develop moral check on employees. As the time between recording and checking is quite short, the staff cannot think to plan any frauds. The auditor at times may surprisingly visit the client’s office, therefore, it will have a considerable moral check.

- Convenient for auditor: The continuous audit is helpful for the audit staff for distribution of work, for the whole year. The audit staff can prepare the programme on the basis of time allocated. The auditor gets sufficient time for important and suspicious matters to draw conclusion.

Disadvantages:

- Small entity: The continuous audit is not fit for small scale business organisations since it has fewer transactions.

- Expensive: It is not suitable for small business organisations with less financial transactions, as the continuous audit is an expensive system of audit.

- Alterations of figures: Figures in the books of accounts which have already been checked by the auditor, may be altered by a dishonest employee and frauds may be committed.

- Disturbance at work: The frequent visits by the auditor may disturb the work of the client. When the audit work starts, the work of accounting staff suffers, as the books are not spare.

Evolution of Auditing

Traditional Audit Era

Historically, audits followed a periodic model:

- Transactions occur

- Financial statements are prepared

- Auditors review historical records

- Audit reports are issued

This approach creates a significant time gap between business events and audit assurance.

Limitations

- Delayed risk detection

- Limited transaction testing

- Heavy manual effort

- High audit costs

- Reactive decision-making

- Sampling risk

Technology-Driven Audit Era

The emergence of:

- ERP systems

- Cloud computing

- Artificial Intelligence

- Machine Learning

- Big Data Analytics

- Process Mining

- Blockchain

has enabled organizations to shift toward real-time assurance frameworks.

Continuous Audit is the result of this technological evolution.

Core Principles of Continuous Audit

1. Continuous Monitoring

Business processes are monitored continuously through automated systems.

Examples include:

- Revenue transactions

- Procurement activities

- Payroll processing

- Inventory movements

- Treasury operations

2. Automated Control Testing

Instead of manually testing controls periodically, systems automatically verify:

- Segregation of duties

- Approval workflows

- Access controls

- Authorization limits

Controls are evaluated every day rather than once a year.

3. Exception-Based Auditing

Auditors focus on anomalies rather than reviewing every transaction manually.

Examples:

- Duplicate payments

- Unauthorized transactions

- Unusual journal entries

- Abnormal vendor activity

4. Risk-Focused Assurance

Resources are directed toward high-risk areas identified through data analytics.

This improves audit effectiveness and efficiency.

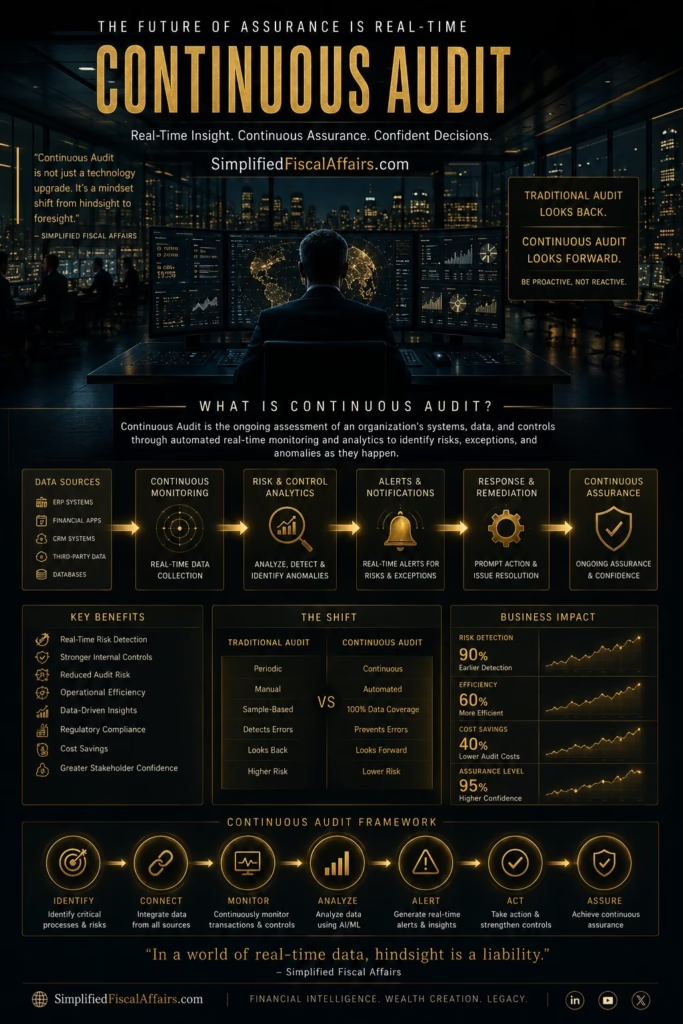

Continuous Audit Framework

Step 1: Data Collection

Data is extracted from:

- ERP systems

- CRM platforms

- Financial applications

- HR systems

- Banking platforms

- External databases

Examples:

- SAP

- Oracle

- Microsoft Dynamics

- Workday

Step 2: Data Integration

Collected information is consolidated into a centralized environment.

Technologies include:

- Data warehouses

- Data lakes

- Cloud platforms

Step 3: Continuous Monitoring

Automated scripts monitor transactions continuously.

Examples:

Accounts Payable

Monitor:

- Duplicate invoices

- Duplicate payments

- Unusual vendors

Payroll

Monitor:

- Ghost employees

- Excessive overtime

- Unauthorized salary changes

Procurement

Monitor:

- Split purchases

- Vendor conflicts

- Policy violations

Step 4: Analytics Engine

Advanced algorithms analyze transactions.

Techniques include:

Descriptive Analytics

What happened?

Diagnostic Analytics

Why did it happen?

Predictive Analytics

What may happen next?

Prescriptive Analytics

What actions should be taken?

Step 5: Exception Detection

When predefined thresholds are breached, alerts are generated automatically.

Examples:

- Fraud indicators

- Compliance violations

- Financial anomalies

Step 6: Investigation and Remediation

Auditors investigate exceptions and management takes corrective action.

Step 7: Continuous Reporting

Dashboards provide real-time visibility.

Reports may include:

- Risk scores

- Control effectiveness

- Compliance status

- Fraud indicators

Continuous Audit vs Traditional Audit

| Feature | Traditional Audit | Continuous Audit |

|---|---|---|

| Timing | Periodic | Real-Time |

| Testing | Sampling | Entire Population |

| Detection | Delayed | Immediate |

| Cost Efficiency | Moderate | High |

| Risk Coverage | Limited | Extensive |

| Automation | Low | High |

| Fraud Detection | Reactive | Proactive |

| Assurance Frequency | Annual/Quarterly | Continuous |

Technologies Powering Continuous Audit

Artificial Intelligence (AI)

AI identifies:

- Fraud patterns

- Risk trends

- Behavioral anomalies

AI continuously learns from historical data.

Machine Learning

Machine learning models improve anomaly detection over time.

Applications include:

- Fraud prediction

- Credit risk analysis

- Transaction monitoring

Robotic Process Automation (RPA)

RPA automates repetitive audit tasks.

Examples:

- Data extraction

- Report generation

- Reconciliation procedures

Benefits:

- Faster execution

- Lower costs

- Reduced human errors

Process Mining

Process mining reconstructs business processes from transaction logs.

It helps auditors identify:

- Control gaps

- Process deviations

- Bottlenecks

Blockchain

Blockchain introduces:

- Immutable records

- Enhanced transparency

- Strong audit trails

Future continuous audit systems may directly interact with blockchain networks.

Continuous Audit Applications

Financial Reporting

Monitoring:

- Journal entries

- Revenue recognition

- Financial close processes

Internal Controls

Continuous evaluation of:

- Access rights

- Approval hierarchies

- System configurations

Regulatory Compliance

Monitoring compliance with:

- SOX

- GDPR

- AML regulations

- Industry-specific requirements

Fraud Detection

Detecting:

- Payment fraud

- Procurement fraud

- Expense manipulation

- Insider misconduct

Cybersecurity

Monitoring:

- Unauthorized access

- Privilege abuse

- Security breaches

Benefits of Continuous Audit

Enhanced Risk Detection

Risks are identified almost immediately.

Organizations can address issues before they escalate.

Improved Audit Quality

Testing entire transaction populations increases assurance levels.

Sampling limitations are reduced.

Stronger Internal Controls

Continuous monitoring encourages control discipline.

Control failures become visible instantly.

Greater Operational Efficiency

Automation reduces manual audit effort.

Auditors spend more time on strategic analysis.

Better Decision-Making

Management receives timely insights.

This improves responsiveness and governance.

Reduced Fraud Losses

Early detection significantly reduces fraud exposure.

Challenges of Continuous Audit

Data Quality Issues

Poor-quality data can generate inaccurate alerts.

Organizations need strong data governance.

Technology Investment

Initial implementation costs may be significant.

Expenses include:

- Software

- Infrastructure

- Training

- Analytics tools

Cybersecurity Risks

Continuous access to systems creates additional security considerations.

Strong controls are required.

Change Management

Employees may resist increased monitoring and transparency.

Proper communication is essential.

Skills Gap

Modern auditors require expertise in:

- Data analytics

- AI

- Programming

- Cybersecurity

- Information systems

Continuous Audit and Artificial Intelligence

The next generation of continuous auditing is increasingly AI-driven.

Future systems may:

- Generate automated audit conclusions

- Predict fraud before occurrence

- Assess control effectiveness autonomously

- Provide real-time assurance opinions

This transformation will move auditors toward higher-value activities such as judgment, governance, and strategic risk assessment.

Real-World Example

Consider a multinational corporation processing 10 million transactions annually.

Traditional Audit

- Sample size: 5,000 transactions

- Review occurs after year-end

- Fraud may remain undetected for months

Continuous Audit

- 10 million transactions monitored

- Real-time anomaly detection

- Immediate alerts generated

- Faster corrective actions

The difference in assurance quality is substantial.

The Future of Continuous Audit

The future is likely to involve:

AI-Powered Assurance

Algorithms continuously evaluate controls and risks.

Blockchain-Based Auditing

Real-time verification of immutable transactions.

Predictive Auditing

Anticipating future control failures before they occur.

Autonomous Audit Systems

Systems that independently perform routine assurance activities.

Integrated Risk Intelligence

Combining:

- Financial risks

- Operational risks

- Cyber risks

- Compliance risks

into a unified assurance framework.

Conclusion

Continuous Audit is not merely an enhancement of traditional auditing—it is a transformational shift in how assurance is delivered. By leveraging automation, analytics, artificial intelligence, and real-time monitoring, organizations can move from reactive auditing to proactive assurance.

As businesses become increasingly digital, interconnected, and data-driven, Continuous Audit is expected to become a cornerstone of modern governance, risk management, and compliance frameworks. Organizations that successfully implement continuous auditing capabilities will gain stronger controls, improved transparency, enhanced fraud detection, and superior decision-making advantages in an increasingly complex business environment.

Disclaimer

The information provided in this article is for educational and informational purposes only and should not be construed as accounting, auditing, legal, regulatory, tax, investment, or professional advice. Readers should consult qualified professionals before making decisions based on the concepts discussed. Continuous audit practices, technologies, and regulatory requirements may vary across jurisdictions, industries, and organizations. SimplifiedFiscalAffairs.com has made sure to provide information with atmost accuracy. Regardless of anything, financial information imparted through this website should not be considered as an offer to make investment decisions.