Finance is a vast subject matter, it is a beautiful language in which investors, businesses and the global economies communicate and interact with. Financial mastery and literacy ultimately impowers one to strategically make the best financial decisions and create the best possible financial outcomes. You are the creator of your reality! Respect the knowledge you are seeking today and tomorrow it will respect you..!

1. Introduction to Financial Risk Management

Financial Risk Management (FRM) is a systematic and scientific approach to identifying, measuring, analyzing, and controlling financial uncertainties that can negatively impact an organization’s value.

At its core, FRM aims to:

Protect capital

Stabilize earnings

Enhance decision-making under uncertainty

In modern finance, FRM evolved from portfolio theory (Harry Markowitz, 1952) and has now become a strategic function, not just a defensive tool.

👉 In simple terms:

FRM ensures that risks are understood, quantified, and managed—not avoided blindly.

2. Nature and Sources of Financial Risk

Financial risk arises due to uncertainty in financial markets, operations, and counterparties.

Key Characteristics:

- Dynamic and interconnected

- Measurable (quantitatively or qualitatively)

- Influenced by macroeconomic and internal factor

3. Types of Financial Risks (Core Classification)

3.1 Market Risk

Risk of losses due to market price fluctuations:

- Interest rate risk

- Foreign exchange (FX) risk

- Equity price risk

- Commodity risk

👉 Example: Rising interest rates reduce bond prices.

3.2 Credit Risk

Risk that a borrower fails to repay obligations.

Includes:

- Default risk

- Counterparty risk

- Settlement risk

👉 Measured via:

- Probability of Default (PD)

- Loss Given Default (LGD)

- Exposure at Default (EAD)

3.3 Liquidity Risk

Inability to meet short-term financial obligations.

Types:

- Funding liquidity risk

- Market liquidity risk

3.4 Operational Risk

Loss due to:

- System failures

- Fraud

- Human error

- External events

3.5 Advanced Risk Types

- Model Risk (errors in risk models)

- Systemic Risk (entire financial system collapse)

- Reputational Risk

- Legal & Compliance Risk

The Ultimate FRM Questionnaire

1. Basic Conceptual Questions

Q1. What is Financial Risk Management?

Answer:

Financial Risk Management is the process of identifying, analyzing and mitigating risks that can affect an organization’s financial health. It ensures stability by balancing risk and return.

Q2. What are the main types of financial risks?

Answer:

- Market Risk

- Credit Risk

- Liquidity Risk

- Operational Risk

Q3. What is Market Risk?

Answer:

Market risk is the risk of losses due to changes in market variables like interest rates, stock prices, exchange rates, and commodity prices.

Q4. What is Credit Risk?

Answer:

Credit risk is the risk that a borrower may fail to meet their financial obligations.

Q5. What is Liquidity Risk?

Answer:

Liquidity risk arises when a firm cannot meet its short-term financial obligations due to lack of cash or inability to convert assets quickly.

2. Intermediate Questions

Q6. What is Value at Risk (VaR)?

Answer:

Value at Risk (VaR) measures the maximum expected loss over a specific time period at a given confidence level.

Example:

If VaR = ₹10 lakh at 95%, there is a 5% chance losses may exceed ₹10 lakh.

Q7. What are the limitations of VaR?

Answer:

- Ignores extreme losses (tail risk)

- Assumes normal distribution

- Not effective during crises

Q8. What is Expected Loss in credit risk?

EL=PD×LGD×EADEL = PD \times LGD \times EAD

Answer:

Expected Loss is the average loss a bank expects from a loan portfolio, calculated using Probability of Default, Loss Given Default, and Exposure at Default.

Q9. What is Risk Appetite?

Answer:

Risk appetite is the level of risk an organization is willing to accept to achieve its objectives.

Q10. What is diversification?

Answer:

Diversification reduces risk by spreading investments across different assets, sectors, or geographies.

3. Advanced / Technical Questions

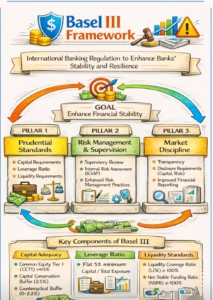

Q11. What is Basel III?

Answer:

Basel III is an international regulatory framework that strengthens bank capital, liquidity, and risk management systems to improve financial stability.

![]()

Q12. What is Capital Adequacy Ratio (CAR)?

Answer:

CAR measures a bank’s capital relative to its risk-weighted assets to ensure it can absorb losses.

Q13. What are Risk-Weighted Assets (RWA)?

Answer:

RWA are assets adjusted based on their risk level. Higher-risk assets require more capital.

Q14. What is Liquidity Coverage Ratio (LCR)?

Answer:

LCR ensures that banks have enough high-quality liquid assets to survive a 30-day financial stress scenario.

Q15. What is stress testing?

Answer:

Stress testing evaluates how financial institutions perform under extreme economic conditions.

4. Case Study-Based Questions (Very Important)

Q16. What caused the 2008 Financial Crisis?

Answer:

- Subprime lending

- Poor credit risk assessment

- Over-reliance on financial models

- Lack of liquidity

👉 It highlighted the failure of risk management systems.

Q17. Why did Lehman Brothers collapse?

Answer:

Lehman Brothers collapsed due to excessive leverage, high exposure to mortgage-backed securities and lack of liquidity.

Q18. What caused the NPA crisis in India?

Answer:

- Poor credit appraisal

- Over-lending to infrastructure sector

- Weak monitoring

Q19. What went wrong in YES Bank?

Answer:

- High exposure to risky loans

- Weak governance

- Misreporting of NPAs

Q20. What lessons were learned from these cases?

Answer:

- Importance of strong governance

- Need for stress testing

- Proper risk assessment is critical

5. Practical / Application Questions

Q21. How do banks manage credit risk?

Answer:

- Credit scoring models

- Collateral

- Diversification

- Monitoring borrower performance

Q22. How is market risk managed?

Answer:

- Hedging using derivatives

- Portfolio diversification

- VaR models

Q23. What is hedging?

Answer:

Hedging is using financial instruments like futures or options to reduce risk exposure.

Q24. What is RAROC?

Answer:

Risk-Adjusted Return on Capital measures profitability after adjusting for risk.

Q25. What is operational risk? Give an example.

Answer:

Operational risk arises from failures in systems, processes, or people.

Example: Fraud or system failure.

6. Analytical / Opinion-Based Questions

Q26. Why is risk management important?

Answer:

It prevents financial losses, ensures stability and improves decision-making.

Q27. Can risk be completely eliminated?

Answer:

No, risk cannot be eliminated, only managed or reduced.

Q28. Which is more dangerous: credit risk or market risk?

Answer:

It depends on context, but credit risk is often more dangerous for banks due to long-term impact.

Q29. How has technology improved risk management?

Answer:

- AI-based risk models

- Real-time monitoring

- Big data analytics

Q30. What is the future of Financial Risk Management?

Answer:

- AI-driven risk analytics

- Climate risk integration

- Stronger global regulations

7. Rapid-Fire (Quick Revision)

- VaR → Maximum expected loss

- EL → Average expected loss

- Basel III → Regulatory framework

- NPA → Non-performing asset

- LCR → Short-term liquidity measure

- RWA → Risk-adjusted assets

🎯 Viva Tip (Very Important)

If the examiner asks unexpected questions, follow this structure:

👉 Define → Explain → Give Example → Link to Case Study

Example:

“Credit risk is the risk of default. For example, during the Indian NPA crisis, banks suffered due to poor credit assessment…”